For years, fintech trends were mostly about making banking look better on a smartphone. Now, the focus has moved to the backend, replacing slow, batch-processed legacy systems with a high-velocity infrastructure that moves money at the speed of data.

The global fintech market is on track to reach 0.76 billion by the end of 2026, growing at a steady 18.20% CAGR. Furthermore, recent market data is even more positive about GAGR and indicates that the broader fintech ecosystem is expected to surge toward a staggering .1 trillion by 2032 .

This explosive growth is being fueled by top fintech trends like the rise of AI agents, the total normalization of real-time payments, and a regulatory landscape that finally caught up with the speed of code.

This evolution is driven by several converging factors:

- The normalization of instant payments: With the widespread adoption of networks like FedNow in the US and the mandates of the Instant Payments Regulation in Europe, liquidity is now instantaneous. This forces companies to rethink everything from payroll to supplier payments.

- The compliance-innovation loop: We’ve entered the "Enforcement Era" for major regulations like DORA and PSD3. Rather than treating these as hurdles, the latest fintech trend is to build compliance directly into the software stack.

- The shift from banking to ecosystems: We are moving away from a world of "standalone" financial products. The future of fintech lies in embedded ecosystems where financial services: lending, insurance, and wealth management are natively woven into non-financial platforms.

Key article takeaways:

- How Agentic AI is replacing traditional chatbots to automate complex financial decision-making

- Why Real-Time Settlement has become the baseline requirement for global B2B and consumer liquidity

- The shift toward Embedded Finance and how non-financial platforms are becoming the new banks

- How to leverage RegTech and Open Finance to turn compliance into a personalized user experience

Read on to discover how these shifts are redefining the financial landscape and what your business needs to do to stay ahead.

The current fintech sector landscape

The current era of fintech is defined by a move away from "isolated apps" toward "integrated protocols". We are creating an autonomous financial layer that sits beneath the entire internet. This transformation is segmented into several high-velocity pillars that prioritize interoperability over walled gardens.

The transition to open finance

While Open Banking focused on sharing transaction data, Open Finance expands this to include mortgages, savings, and pensions. This allows for a "holistic balance sheet" view, enabling AI agents to manage a user’s entire net worth automatically across different platforms.

Always-on treasury and liquidity

For the enterprise, the "business day" is becoming a relic. Real-time settlement rails (like SEPA Instant or FedNow) are merging with programmable treasury tools, allowing companies to move liquidity across borders at 3:00 AM on a Sunday without human intervention.

The rise of agentic commerce

We are moving past simple "one-click" checkouts into a world of delegated authority. In this model, AI agents, not humans, are the ones making purchasing and investment decisions based on pre-set parameters and real-time market data.

Institutional digital assets (tokenization)

This isn't about retail crypto speculation. It is about "Real-World Asset" (RWA) tokenization, putting treasury bonds, real estate, and carbon credits on-chain to enable fractional ownership and instant collateralization.

According to the KPMG 2026 Pulse of Fintech report , "Digital assets and tokenization will likely be the big narrative in 2026. Corporates are increasingly using digital assets for money market funds, treasury management, and payables and receivables". This institutionalization of tech-native finance marks the end of the "experimentation" phase.

This systemic re-architecture is what allows fintech technology trends to scale globally. By standardizing the "plumbing" of finance through APIs and smart contracts, a startup in Lagos can now access the same institutional liquidity and security protocols as a hedge fund in Manhattan.

In this environment, fintech industry trends are increasingly dictated by "compliance-as-code". Regulators are plugging directly into the data streams of fintechs to monitor risk in real-time. This reduces the "compliance tax" on innovation while simultaneously hardening the system against systemic shocks.

Ultimately, the most successful trends in fintech over the next 24 months will be those that solve the "trust gap". As AI handles more of our money, the premium moves from the technology itself to the governance and transparency surrounding it. The goal is no longer just to make finance digital, but to make it fundamentally more reliable and equitable than the legacy systems it replaces.

Top fintech industry trends you should know in 2026

The biggest fintech trends are about re-engineering the very plumbing of the global economy. From autonomous AI agents to the tokenization of real-world assets, the following list outlines the ten pillars currently redefining the sector.

- Agentic AI: From assistance to autonomy

The fintech sector has graduated from passive "chatbots" to Agentic AI — autonomous systems capable of navigating complex financial workflows without human intervention. Unlike traditional AI that merely suggests actions, these agents possess "agency" to negotiate payment terms, optimize currency conversions, and execute cross-border transfers based on high-level liquidity goals.

For the end-user, this means a shift from "do it for me" to "it’s already done". For the business, it represents a total decoupling of operational scale from headcount, allowing a lean startup to manage thousands of complex treasury operations that once required a massive back-office team.

Why does it matter today?

With the proliferation of real-time payment rails and 24/7 liquidity markets, the "human-in-the-loop" has become a bottleneck. The push toward autonomous agents is driven by a need for hyper-efficiency, as the global fintech market is expanding to a scale that is physically impossible to manage without automated decision-making layers. According to the Wolters Kluwer's research, the adoption rate is skyrocketing: "44% of finance teams will use agentic AI in 2026, representing an increase of over 600%" compared to previous years.

From an engineering perspective, this requires a transition from traditional request-response architectures to event-driven autonomous workflows.

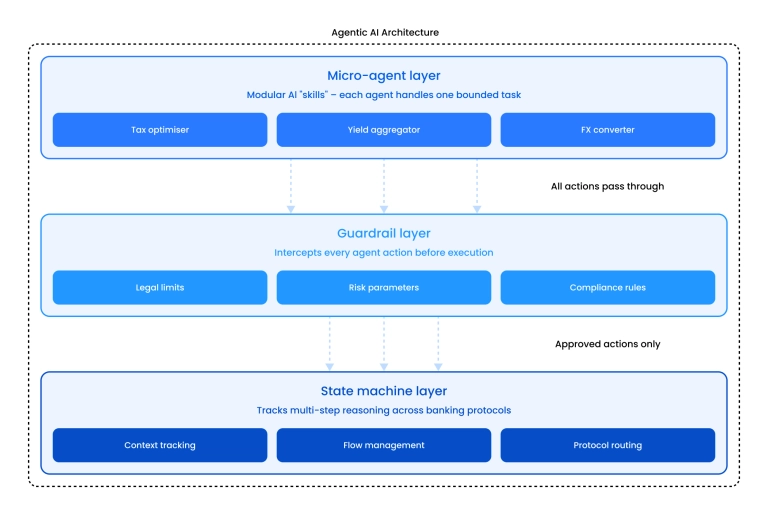

- Micro-agents: Development focuses on building modular "skills" for AI agents (e.g., a "tax-optimizer" skill or a "yield-aggregator" skill).

- Guardrail layers: Architecture must include hard-coded "guardrail" services that intercept agent actions to ensure they remain within legal and risk parameters.

- State machines: Complex state management is required to track the multi-step reasoning of an agent as it navigates through different banking protocols.

Binariks helps firms bridge the gap between "smart" and "autonomous". We specialize in building the secure API middleware and event-driven architectures necessary for AI agents to operate safely.

For example, our team engineered a cloud-native model execution platform that drastically improved processing speed and deployment agility, providing the foundational low-latency environment required for autonomous financial agents to execute real-time transactions.

- Invisible (embedded) finance 2.0

Embedded finance has graduated from simple "payment buttons" into its Invisible 2.0 phase, where complex financial services, lending, insurance, and wealth management, are native, background functions within non-financial ecosystems. Whether it's a logistics platform offering instant cargo insurance or a healthcare portal providing automated patient financing, the financial transaction is now a seamless byproduct of the primary user activity.

This shift strips traditional banks of their front-end monopoly. In this new value chain, the "software layer" (the SaaS or marketplace) owns the customer relationship and data, while the bank is relegated to a regulated utility provider. For businesses, this means higher customer "stickiness" and the ability to monetize existing user bases without the overhead of becoming a licensed financial institution.

Why does it matter today?

According to research by Bain&Company, the transaction value of embedded finance is projected to exceed trillion by 2026 , accounting for over 10% of all US financial transactions.

The growth is particularly aggressive in non-retail sectors. Recent data from Mordor Intelligence indicates that while retail still leads, the healthcare and pharmaceuticals segment is advancing at a 26.1% CAGR through 2031 . This is driven by the urgent need for "contextual" finance — services that appear precisely when a financial hurdle arises in a non-financial journey.

Binariks specializes in the deep architectural integration required to make finance truly invisible. We help companies navigate the "Compliance-as-Code" requirements of embedded services while maintaining high-velocity performance.

For example, we helped a primary care platform modernize its data infrastructure, integrating disparate Medicare sources to enable the real-time data flow necessary for seamless insurance verification and integrated patient care.

- Real-world asset (RWA) tokenization

Real-World Asset (RWA) tokenization, the process of digitizing ownership of tangible assets like real estate, gold, and government bonds, has become the standard for unlocking liquidity in traditionally illiquid markets. By converting these assets into programmable tokens on a distributed ledger, the industry enables fractional ownership and near-instant settlement cycles that were previously impossible.

For investors, this democratizes access to "whales-only" asset classes like private equity or commercial skyscrapers. For financial institutions, it eliminates the "paperwork tax", replacing weeks of manual verification with smart contracts that handle compliance, dividends, and ownership transfers automatically.

Why does it matter today?

We have reached an inflection point where institutional demand meets regulatory clarity. According to a 2026 thematic outlook by BlackRock, tokenization is now recognized as a "fundamental reengineering of financial market infrastructure". This aligns with the widely cited projection from Boston Consulting Group (BCG) that "tokenized fund AUM could reach 1% of global mutual fund and ETF AUM by 2030", implying a valuation of over 0 billion in that segment alone, as part of a broader $16 trillion opportunity across all illiquid assets.

Binariks provides the high-performance engineering required to turn physical assets into digital opportunities. We specialize in building the secure, compliant foundations for tokenization platforms. We provide blockchain development services and create custom asset tokenization platforms that allow businesses to trace and transfer ownership rights seamlessly while maintaining full regulatory alignment.

- Real-time everything: The end of "business days"

The concept of a "three-to-five business day" waiting period for cross-border payments is becoming a relic of the past. The global economy has shifted to real-time everything, where liquidity is 24/7/365 and transactions settle in seconds.

For businesses, this means the end of "trapped capital". Instant settlement frees up massive amounts of working capital that was previously held in clearinghouse limbo. For consumers, it enables "just-in-time" financial lives, getting paid for a gig the second the task is finished or avoiding late fees through instant, automated transfers.

Why does it matter today?

Real-time rails like FedNow in the U.S. and the maturity of the SEPA Instant mandate in Europe have made 24/7 liquidity a baseline expectation. According to a 2026 analysis by ACI Worldwide, the volume of real-time transactions is expected to exceed 511 billion annually by 2027, representing a five-year CAGR of over 30%.

This shift is fundamentally changing corporate behavior. Real-time liquidity is now a "top-three priority for corporate treasurers", as firms look to optimize cash forecasting in an era of higher interest rates.

Binariks provides the high-performance engineering needed to maintain 24/7 uptime in a real-time world. We specialize in building the high-load, cloud-native infrastructures required to handle instantaneous data and transaction flows. For example, Binariks modernized the data infrastructure for a nationwide provider , utilizing AWS and Snowflake to ensure real-time connectivity and high-speed data processing.

- The transition from open banking to open finance

While its predecessor, open banking, was limited to payment and account data, open finance brings insurance, pensions, mortgages, and investments into the API ecosystem. This evolution creates a "360-degree digital financial identity", allowing for a unified view of a user's entire net worth across disparate platforms.

This transition turns the "bank account" into just one node in a larger web. For consumers, it enables hyper-personalized financial advice and the ability to instantly switch providers for better mortgage rates or pension yields. For businesses, it unlocks massive cross-selling opportunities and the ability to build "super-apps" that manage every facet of a user’s economic life.

Why does it matter today?

The European Commission’s Financial Data Access (FiDA) regulation and the UK’s Data (Use and Access) Act have set clear deadlines for data sharing across non-payment sectors. According to Mastercard’s 2026 Open Finance report, the stakes are high: "76% of consumers are now ready to switch financial providers for better digital money-management features", and companies that have successfully bridged data gaps report an average 7.5% revenue uplift.

Binariks helps traditional and digital-first firms capitalize on the API economy by building the secure, scalable foundations required for open finance. We specialize in re-architecting legacy systems into cloud-native, API-centric ecosystems that can securely handle high-volume data exchanges.

- Biometric identity and "proof of personhood"

As generative AI makes traditional "Know Your Customer" (KYC) processes vulnerable to sophisticated deepfakes, the industry is pivoting toward hardware-level biometric authentication and Decentralized Identity (DID). This trend shifts the anchor of trust from easily phishable passwords or SMS codes to "Proof of Personhood," where a user’s financial identity is tied to secure enclaves on their physical devices and verifiable credentials on a ledger.

This effectively ends the era of centralized "identity honeypots". Instead of banks storing millions of sensitive social security numbers in a single database, users hold their own "keys". For businesses, this drastically reduces the liability of data breaches and eliminates the friction of repeated identity verification.

Why does it matter today?

Synthetic identity fraud, which involves creating "Frankenstein identities" from real and fabricated data, has become the top threat for financial institutions. According to the 2026 Synthetic Identity Fraud Report, "Financial-sector identity fraud is surging, with identity theft generating 12% of total losses from just 7% of cases, pointing to much higher loss severity per incident".

The shift is further accelerated by the global adoption of reusable digital credentials. Research from Gartner predicts that "at least 500 million smartphone users will regularly make verifiable claims using a digital identity wallet built on distributed ledger technology by 2026".

Furthermore, market data from SQ Magazine indicates that identity vendors are now "detecting more than 1 million deepfake attempts monthly in high-risk sectors", making passive liveness detection and biometric hardware-binding a non-negotiable requirement for digital banking.

Binariks helps companies build ironclad security frameworks that exceed modern compliance standards. We specialize in implementing advanced identity management and multi-factor authentication (MFA) within complex cloud environments. For example, Binariks delivered a secure messaging platform based on ID verification, ensuring that sensitive identity verification was handled with maximum security and full GDPR compliance.

- Green fintech and programmable ESG

Green Fintech refers to the integration of environmental, social, and governance (ESG) metrics directly into financial products, ranging from carbon-footprint trackers in consumer banking to AI-driven ESG risk scoring for institutional portfolios.

Sustainability is transitioning from a "feel-good" marketing feature to a hard financial metric. A company’s carbon footprint directly impacts its cost of capital. For fintechs, the latest trends in fintech suggest that "green" elements must be programmable, automatically adjusting interest rates or investment allocations based on real-time environmental data.

Why does it matter today?

Regulatory mandates have turned ESG reporting into a non-negotiable requirement for financial institutions. By 2026, the Corporate Sustainability Reporting Directive (CSRD) has matured, making granular data transparency a global baseline.

According to a 2026 industry analysis by IntellectAI, the momentum is quantifiable: "ESG FinTech is projected to attract 3.7 billion in investment by 2026", as firms race to meet evolving regulatory requirements and capitalize on the demand for sustainable services.

- RegTech as a competitive moat

In the high-velocity world of instant payments, Regulatory Technology (RegTech) has transitioned from a back-office cost center to the hottest fintech trend for achieving operational excellence. It has evolved into a real-time defense layer where "compliance-as-code" integrates regulatory rules directly into transaction logic.

Modern RegTech turns this on its head by automating the "boring" parts of regulation, fintechs can launch products faster and move into new jurisdictions with lower risk.

Why does it matter today?

The volume and complexity of global mandates have reached a critical threshold, making manual oversight a liability rather than a strategy. According to the 2026 RegTech Market Report by Future Market Insights, the global sector is on track to reach a valuation of .1 billion in 2026 , with software solutions commanding a dominant 58.5% share due to their "unmatched efficiency in automating compliance with evolving regulations".

AI-powered RegTech is delivering massive productivity gains, with Dataintelo noting that these modules are "reducing the average compliance team response time from 14 days to under 48 hours ".

Binariks helps fintechs build products that are "compliant by design." We specialize in integrating automated KYC, AML, and reporting workflows into cloud infrastructures.

- Account-to-account (A2A) payments maturity

By bypassing traditional card networks to move funds directly between bank accounts via open banking APIs, "Pay by Bank" offers a one-click experience that rivals digital wallets. This shift is a key latest trends in fintech driver, fueled by the maturation of real-time settlement rails and a collective push from merchants to escape rising interchange fees.

For merchants, A2A is a strategic margin protector, reducing transaction costs by 15–20% compared to legacy card infrastructure. For consumers, it eliminates the friction of manual card entry and expiration dates, providing instant, secure confirmation of cleared funds.

Why does it matter today?

A2A has officially entered the mainstream, catalyzed by the EU’s Instant Payments Regulation and the global success of real-time schemes like Pix and UPI. Analysts at Visa project that the global consumer A2A market will surge from 60 billion transactions in 2024 to more than 185 billion by 2029, marking a massive 209% increase in just five years.

This transition is further supported by another research , which notes that in 2026, the technical friction that once held A2A back has vanished, allowing bank transfers to match the conversion rates of global card schemes.

Binariks builds the high-load API integrations required to connect diverse banking ecosystems. We specialize in developing interoperable payment gateways that handle real-time settlement with extreme reliability. For example, Binariks delivered a secure ID authentication and messaging platform that seamlessly integrated Swedish BankID, a critical component for the secure, one-click authentication that defines modern A2A payment flows.

- Hyper-personalization via predictive intelligence

Fintech is moving from a reactive ledger model to a proactive new fintech trend known as Predictive Intelligence. By utilizing generative AI to analyze datasets like social sentiment and supply chain telemetry, platforms now forecast rather than just report. This enables Just-in-Time financing, identifying cash-flow gaps weeks in advance to offer pre-approved liquidity before a crisis occurs.

This turns banks into financial coaches for consumers and digital CFOs for businesses, automating responses to market volatility and optimizing treasury management.

Why does it matter today?

A Gartner analysis states that generative AI will become the top disruptor for the banking industry by 2026, with analytics leading credit scoring. Research from The Financial Brand shows institutions see a 14% increase in customer lifetime value through tailored products. Additionally, IBM reports that specialized small data models now offer 98% accuracy in SME expense forecasting.

Engineering requires Feature-Store Architectures and Streaming ML Pipelines for real-time data processing. Systems must utilize Vector Databases to manage the high-dimensional data needed for similarity searches that drive personalized recommendations.

Binariks builds high-performance pipelines for modern AI. We created a cloud-native model execution platform for a financial provider, slashing deployment times to enable complex, real-time predictive models at scale.

Related Case Study

Transforming Fund Administration with AI: How a Global Asset Manager Achieved 90% Processing Time Reduction

Cloud Migration That Cut Deployment Time by 96% and Enabled Daily Releases

From Bottleneck to Breakthrough: Scaling Loan Management to 999 TPS and 6 Million Monthly Disbursements

Secure Messaging Platform Based on ID Authentication

Transforming Fund Administration with AI: How a Global Asset Manager Achieved 90% Processing Time Reduction

Binariks developed an AI-driven document processing solution for a global asset management firm. Built on Azure AI with custom ML models and automated validation workflows, the system reduced fund administration report processing time by 90%, eliminated 75% of manual errors, and enabled scalable, cost-efficient operations.

The challenge of implementing fintech trends

The real bottleneck for the trends of fintech isn't the code, it’s the "black box”. We’ve moved past the novelty of autonomous finance and into an era of governed intelligence. The industry is currently locked in a battle for explainability, where a fintech’s ability to justify its AI’s decisions is the only thing standing between a market lead and a massive regulatory fine.

To navigate these tech trends in fintech, leaders are moving beyond isolated tools toward three strategic survival shifts:

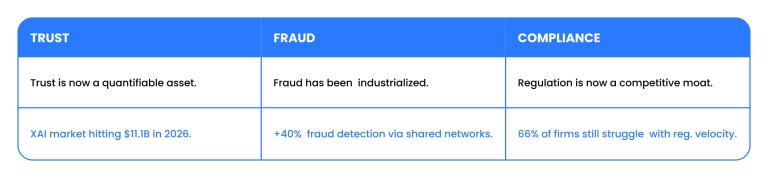

- Trust is now a quantifiable asset. With the global explainable AI (XAI) market projected to hit $11.1 billion this year, "because the algorithm said so" is no longer a valid legal or customer response. Modern systems must now generate "explainability artifacts", plain-language justifications for every automated loan denial or fraud flag, to satisfy maturing global frameworks like the EU AI Act.

- Fraud has been industrialized. Deepfake-powered synthetic identities are launching attacks that no single institution can defeat alone. The current move is toward "consortium analytics", where firms share real-time security signals across a global network. According to Plaid, participating in these shared defense layers can boost first-party fraud detection by up to 40%, turning a solitary defense into a collective immune system.

- Regulation is being reframed from a "brake" into a competitive moat. While 66% of organizations still struggle with the velocity of regulatory change, the winners are using "compliance-as-code" to automate the grunt work. This is about creating a transparent, audit-ready infrastructure that secures investor confidence and allows for aggressive scaling into new jurisdictions.

How Binariks helps you leverage fintech trends

Staying ahead of IT trends in fintech is about architecting systems that don't crumble under the weight of new regulations or sophisticated fraud. Binariks acts as the engineering backbone for firms transitioning from legacy constraints to the high-stakes world of autonomous, real-time finance. We solve the explainability crisis and the compliance crunch by turning disruptive trends in the fintech industry into defensible, production-grade realities.

Our approach focuses on building "trust-first" architectures that prioritize data integrity and transparency. For a global asset management leader, we engineered an AI-powered solution that reduced manual processing by 90% while ensuring every automated decision was backed by a clear audit trail.

Similarly, we helped a Swedish fintech bridge the security gap by delivering a secure messaging platform integrated with national BankID, turning complex identity verification into a frictionless competitive advantage.

- Audit-ready AI: We build the reasoning layers required to turn "black-box" models into transparent, compliant agents.

- Network-scale defense: Our engineers integrate biometric identity (DID) and consortium-based signals to counter industrialized fraud.

- Compliance-as-code: We automate regulatory oversight within the data pipeline, allowing for rapid scaling into new jurisdictions.

- Cloud-native agility: We re-architect legacy stacks into event-driven systems that can process 24/7 real-time settlement rails.

The era of isolated digital apps is over, replaced by a hyper-connected ecosystem where compliance is automated, identity is biometric, and liquidity is instant. For firms to thrive, the focus must shift from simply building features to mastering the underlying data orchestration that makes finance invisible, autonomous, and above all, trusted.

Wrapping up with fintech trends

By 2026, the IT trends in the fintech industry have coalesced into a singular reality: finance is no longer a destination, but a seamless layer of the digital experience.

We have moved past the era of "digital-first" banking and into the era of industrial-grade autonomy, where the success of a platform is measured by how little the user has to think about the underlying transaction.

The winners of 2026 are not those with the flashiest UI, but those who have mastered three core domains:

- The Explainability Standard: As AI agents take over operational decision-making, "trust" has become a technical requirement. Systems must be built with transparency by design, providing clear audit trails that satisfy both the end-user and the global regulator.

- Real-Time Everything: With the maturity of A2A payments and instant settlement rails, the window for error has vanished. Development must focus on low-latency, high-concurrency architectures that can handle the 24/7 liquidity demands of a global economy.

- Ecosystem Interoperability: Whether through Embedded Finance or Open Banking APIs, your product must be "plug-and-play." Success in 2026 requires building modular, extensible stacks that can seamlessly integrate with non-financial platforms and shared defense networks.

The next phase in the latest technologies in fintech software development is about moving from "disruption" to "stability". It’s about building systems that are as resilient as they are innovative.

At Binariks, we provide the architectural depth and engineering precision to turn these high-level shifts into your long-term competitive moat. The future of finance is already here, it’s just waiting to be engineered.