Someone files a car insurance claim on a Saturday afternoon and assumes they'll hear back before the work week starts. That assumption is new. A decade ago the same person would have mailed a form and waited a fortnight without complaint.

Somewhere in between, customer experience in insurance quietly rewrote its own rules, and plenty of carriers didn't notice until policyholders started walking over a slow app. Customer experience now drives retention and growth, rather than sitting off to the side as a service-desk concern.

At Binariks, we build the systems underneath all of this: the self-service portals, the claims automation, the underwriting engines that decide whether a customer waits ten minutes or ten days, through our insurance software development services .

Most insurers we talk to are already sold on the idea that experience matters. Their real problem is narrower and more annoying: with a finite budget, what do you fix first?

After reading this article, you will know:

- How the insurance customer journey really flows, and the one stage where carriers tend to lose people

- What personalization at scale takes, beyond dropping a first name into an email subject line

- Where AI-enabled servicing and claims automation change what policyholders expect

- Which platforms, strategies, and metrics separate the insurers who are improving from the ones who aren't

Most of the insurance customer experience trends worth tracking in 2026 come back to the same place: the distance between what the journey promises and where it actually falls apart. That gap is where how to improve customer experience in insurance stops being a talking point and turns into a plan.

What is customer experience in insurance?

Insurance customer experience is the sum of every interaction a policyholder has with an insurer — from the first quote to a claim payout years later. It spans four main components: digital touchpoints (apps, portals, chatbots), human touchpoints (agents, adjusters, support), the claims process, and ongoing policy servicing.

What makes insurance CX uniquely challenging is the trust gap at its core: customers pay premiums for years, often without a single meaningful interaction, and then judge the entire relationship in one high-stress moment — usually a claim. That moment is rarely neutral. It happens after an accident, a health crisis, or a property loss, which means emotional stakes are high and tolerance for friction is near zero.

In 2026, the bar has shifted. Customers no longer benchmark insurers against other insurers — they benchmark them against Amazon, their bank's mobile app, and same-day delivery. Slow claims, paper-heavy onboarding, or a generic renewal email now feel like active failures, not just missed opportunities. At the same time, AI-powered underwriting and embedded insurance have compressed the purchase journey to minutes, making the post-sale experience the primary differentiator.

Why CX has become a competitive differentiator in insurance

For most of its history, insurance competed on two things: price and coverage. That era is closing. When a policyholder can pull a quote from four carriers before lunch and read every review on the way, the product stops being the only battleground and the experience around it becomes the tiebreaker.

That shift is why the importance of customer experience in insurance has stopped being a slogan: PwC found 73% of consumers call experience an important factor in what they buy, and that they will pay a premium of up to 16% for a good one.

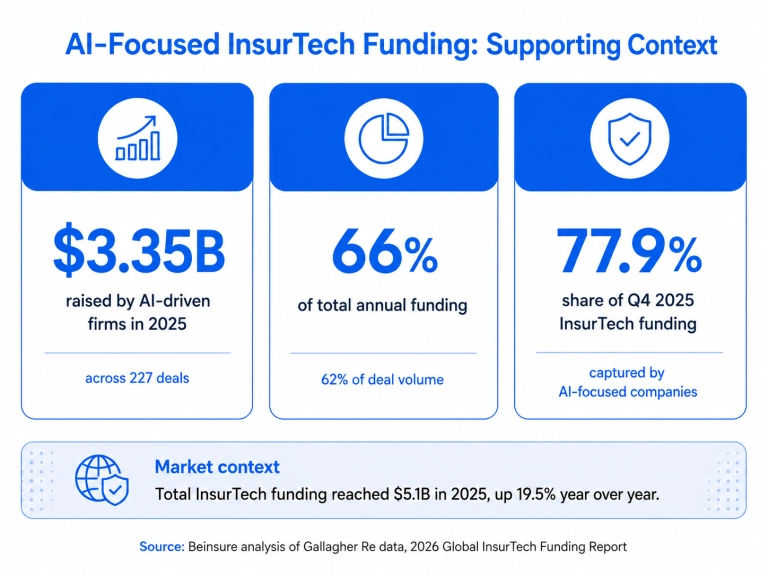

This paradigm shift is fueling massive technical investments across the sector. The global artificial intelligence in insurance market size is projected to scale aggressively from USD 14.39 billion in 2026 to nearly USD 176.58 billion by 2035, highlighting how critical automated experiences have become to carrier survival.

A customer might touch their insurer twice a year, and one of those times they are stressed, filing a claim after a crash or a break-in. Fumble that moment and the relationship is usually over. The carriers that get the insurance customer journey right are quietly taking customers from the ones that don't, and the gap is measurable.

According to the Deloitte 2026 Global Insurance Outlook, 51% of life insurance customers give their insurer a top rating for trust. At some carriers, that drops to 33%. Trust is the whole product in life insurance, so a third of customers at the weaker carriers not feeling it is not a soft problem. It is churn waiting to happen.

What "good" looks like depends on the line of business, and treating all three the same is a common mistake. The priorities split cleanly:

- Auto and property: speed and slick self-service. Customers want the claim handled on their phone in minutes and the money in their account without a follow-up call, and they judge the insurer on how little friction stands in the way;

- Life: trust and human guidance. These are decisions about family and money, and a chatbot pushed into the wrong moment reads as tone-deaf, not helpful

- Health: a blend of both, pairing fast digital admin for routine tasks with human support for the moments that genuinely need a person.

Map your customer journey insurance industry strategy onto these differences, because a life insurer copying an auto insurer's playbook will alienate the exact customers it most needs to keep.

If you trace most insurance customer experience trends heading into 2026 back to their root, they land on the same touchpoint: claims. It is where loyalty is won or lost. We rebuilt one carrier's first notice of loss process from scratch — the single interaction most likely to decide whether a customer renews or walks. You can see how we approached it in our FNOL case study .

The modern insurance customer journey

The insurance customer journey is the full path a policyholder travels with an insurer, across six stages: awareness, quote, purchase, policy management, claims, and renewal. Each stage spans multiple channels (web, app, agent, call center) and each one is a chance to keep the customer or lose them. The journey is rarely linear, and the stages that feel routine to the insurer, like a claim, are often the most emotionally charged for the customer.

Mapping the insurance customer journey end to end is the first thing we do with any carrier, because you cannot fix what you cannot see. Each of the six stages is its own make-or-break moment:

- Awareness. The customer realises they need cover, prompted by a life event, a renewal notice, or a competitor's ad. First impressions form here, often before they ever contact you.

- Quote. They compare options, increasingly through digital channels. A slow form or too many questions loses them to the carrier with the smoother quote.

- Purchase. The moment of commitment. Hidden fees, a clunky checkout, or a confusing policy summary turn a near-win into an abandoned cart.

- Policy management. The long, quiet stretch between purchase and claim. Customers want to update details, add a driver, or check coverage without phoning anyone. Self-service either earns trust here or slowly erodes it.

- Claims. The moment of truth. This is where the promise of insurance is finally tested, and where the customer is most likely to be stressed and paying close attention. A claim handled fast and humanely buys years of loyalty. One that drags, confuses, or feels adversarial undoes every smooth interaction that came before it. Get the insurance claim customer journey wrong and the renewal is already gone, whatever the price.

- Renewal. The decision to stay or leave. It is shaped almost entirely by everything before it, and the last claim weighs heaviest of all.

Notice that the claim sits in the middle of the journey but decides the end of it. That is why it carries more weight than the other five stages combined, and why so much of the work we do with insurers concentrates there.

Journey orchestration: from fragmented touchpoints to one continuous conversation

Most insurers manage each stage in isolation — the quote team doesn't see the claim history, the renewal system doesn't know the customer called support three times last month. Journey orchestration fixes that. It is the practice of connecting every channel and every interaction into a single real-time view of the customer, then automatically triggering the right response at the right moment.

In practice, this means: if a customer opens the claims portal at 11pm, an orchestration layer recognizes the event, logs it against their profile, and queues a proactive status update for the next morning — without a human making that call.

If a high-value policyholder misses a renewal payment, orchestration routes them to a retention specialist rather than an automated dunning sequence. The system reads behavioral signals and responds across web, app, agent, and call center as if it were one continuous conversation.

Orchestration closes the gap between a customer journey insurance industry map that looks good on paper and one that actually feels good to the customer living through it. Done well, it turns reactive service into anticipatory care — which is what policyholders now expect and rarely get.

Personalization at scale: How insurers are doing it

Personalization in insurance used to mean printing the customer's first name at the top of a renewal letter. Today it means an insurer that knows a policyholder renewed their auto cover last month, has a teenage driver, and lives in a postcode that flooded in spring, and that shapes every offer, price, and message around those facts in real time. The gap between the two definitions is where the market is splitting.

The size of that gap is striking. Only about one in four insurers can deliver personalization at scale today, while 60% of customers say they would switch carriers for a more personalized experience, not for a lower premium. A personalized insurance experience at this level rests on three capabilities, and most carriers have gaps in at least one. Roughly three-quarters of the industry is handing the most valuable customers a reason to leave.

Data-driven policy customization

The foundation is using behavioral and contextual data to shape the actual policy, not just the marketing wrapper. Telematics adjusts an auto premium to how someone really drives. IoT sensors price a home policy on whether the smoke detector works. Wearable and wellness data shapes health cover.

This is the engine behind real-time, data-driven underwriting, the kind we built when we cut one insurer's underwriting time from 15 days to minutes in our AI underwriting work . The hard part is rarely the model. It is feeding the model clean data, which is why most carriers stall here.

Real-time offers & next-best-action

The second capability is acting on data in the moment. A next-best-action engine watches what the customer is doing right now, browsing a quote, adding a driver, opening a claim, and surfaces the single most relevant offer or message for that exact context, rather than blasting the same campaign at everyone.

Hyper-personalization in insurance

The leading edge is hyper-personalization: treating every policyholder as a segment of one, across every channel, continuously. The ambition, as carriers like IAG describe it, is a connected experience where each touchpoint carries the context of the last, so a customer never has to repeat themselves and never gets a tone-deaf offer.

This is also where insurance personalization collides with governance, because the more behavioral the data, the heavier the privacy and regulatory load (GDPR and the EU AI Act in Europe, a patchwork of state laws in the US). The carriers pulling ahead build that privacy architecture in from the start, rather than bolting it on once regulators come knocking.

Currently, Large Language Models (LLMs) lead adoption velocity within operations and claims processing at a 65% utilization rate, while predictive machine learning models anchor 54% of sales and underwriting pipelines.

AI-enabled servicing and claims automation

If claims is where loyalty is won or lost, AI is what now decides the outcome. The same technology shows up across four jobs in a modern insurer, each aimed at a moment customers actually judge you on. Together they are what insurance customer experience automation looks like in practice: not a chatbot bolted onto a website, but intelligence threaded through the whole servicing chain.

Automated claims processing

AI can take a claim from first notice of loss through documentation to a decision with minimal human touch: reading uploaded photos, classifying damage, pulling data from forms, and routing clean cases straight to approval while flagging the messy ones for a human.

We built this for an EU insurer in our AI-powered car insurance app . Their damage assessment was manual and slow, which frustrated policyholders and capped how many claims brokers could process. Starting with an R&D phase on their existing claims data, our team trained a computer-vision model that identifies the damaged car part from an uploaded photo, classifies the damage across six types, and estimates repair cost in real time.

The result: far faster assessments, automatic approval of minor claims, and a sharp drop in manual reviews, with the app now in active use across a wide market.

AI chatbots and virtual agents

Most customer questions are routine: claim status, a document upload, a change of address. AI chatbots handle those instantly, at 3am, in any language, without a queue.

The skill is knowing when to hand off: a good system resolves the simple things and routes the emotional or complex ones to a person with full context attached, so the customer never repeats themselves. Used this way, automation removes friction instead of building a robotic wall in front of help.

Fraud detection through ML

Fraud is a tax every honest policyholder pays through higher premiums, and it is one of the strongest cases for machine learning in insurance. ML models spot patterns a human reviewer misses across millions of claims, flagging the suspicious ones while letting legitimate claims move faster.

As Deloitte notes in its 2026 Global Insurance Outlook, real-time, AI-driven fraud analytics could save P&C insurers up to USD 160 billion by 2032. Better fraud detection is also better CX, because it clears honest customers faster instead of holding everyone up.

Automated underwriting

Underwriting used to mean days of waiting. AI compresses it by pulling and assessing risk data in real time, so a customer gets a decision while they still want the policy, not a week later when the urgency has gone.

This is where AI analytics for customer experience in insurance pays off twice: the same models that price risk accurately also surface the insight that powers personalization and proactive service. Speed for the customer, sharper risk selection for the insurer.

Digital customer experience platforms for insurance

A digital customer experience platform for insurance is the connected software layer that runs every policyholder interaction across web, mobile, and agent channels from one place. Its core capabilities are a unified customer profile (one view of the policyholder across products and touchpoints), omnichannel servicing, self-service policy and claims management, real-time personalization, and analytics that feed the whole loop.

The reason carriers are pouring money into these platforms is simple, and a little uncomfortable. US insurance technology spending is set to rise by USD 173 billion in 2026, up 7.8% on the year, and Forrester is blunt about why: CX scores for auto and home insurers are falling even as premiums climb.

Customers are paying more and enjoying it less, and a strong digital experience insurance platform is how carriers close that gap before churn does it for them.

A good platform makes the digital experience in insurance feel like one conversation rather than a relay race between disconnected systems. That is the whole promise of an omnichannel insurance experience: the quote a customer starts on their laptop is waiting on their phone, the agent who picks up the call already sees the half-finished claim, and every channel draws from the same profile.

The strategic question is rarely whether to invest, but how. Most carriers land on one of two paths, and each has real trade-offs:

| Feature | Off-the-shelf platform | Custom-built platform |

| Speed to launch | Fast: live in weeks or months | Slower: built around your needs |

| Cost shape | Lower upfront, ongoing license fees | Higher upfront, lower long-run per-user cost |

| Fit to processes | You adapt to the software | The software adapts to you |

| Differentiation | Same tools your competitors use | A genuine experience edge |

| Legacy integration | Limited by vendor connectors | Built to fit your exact stack |

| Best for | Standard workflows, fast starts | Complex products, legacy systems, scale |

The honest answer is that many insurers end up somewhere in between, buying a core and customizing the layers that touch the customer. The deeper your legacy systems and the more your product differs from the standard mould, the more a custom build pays off, which is the work we focus on in our platform development practice.

The whole point of insurance digital transformation customer experience is that the platform should bend to your business and your policyholders, not force both to bend to a vendor's roadmap.

How to improve customer experience in insurance: Key strategies

You improve customer experience in insurance by fixing the touchpoints customers actually judge you on, in order of impact: orchestrate the journey across channels, automate claims with AI, personalize with behavioral data, and give customers self-service plus proactive communication, then measure the result at each step.

The single highest-return move is usually the claim, because it is where loyalty is decided. The thread connecting all of them is treating experience as infrastructure, not a campaign.

The stakes are not subtle. 64% of consumers would consider switching insurers purely for a better digital experience. Here are seven strategies that move the needle, roughly in order of impact.

- Implement omnichannel journey orchestration. Connect web, app, agent, and call center so the customer's context follows them everywhere. The same Insurity research found only 15% of customers want a fully digital-only experience while 48% want digital-first with a human on standby, so orchestration is about smooth handoffs between channels, not replacing people with bots.

- Automate claims with AI, from FNOL to settlement. Claims is the moment of truth, so it earns the most attention. AI that reads photos, classifies damage, and auto-approves clean cases turns a multi-day ordeal into a same-day resolution, while routing the complex claims to humans with full context.

- Use behavioral data for personalized offers. Move past the customer's first name to telematics, IoT, and life-stage signals that let you price fairly and recommend what is actually relevant. Done well, this is how you enhance customer experience in insurance without it feeling like a sales push.

- Build self-service portals. Let customers manage policies, update details, upload documents, and track claims without phoning anyone, on their schedule, at any hour. Self-service handles the routine so your people are free for the moments that genuinely need them.

- Communicate proactively at renewal and after claims. Silence is where trust leaks out. A heads-up before a premium changes, a status update mid-claim, a check-in after settlement: these small, well-timed messages are the cheapest loyalty you can buy.

- Measure CX at key journey touchpoints. Track NPS, CES, and CSAT not as a single annual score but at each stage, quote, claim, renewal, so you can see exactly where the journey breaks and fix that, rather than guessing. Improving customer experience in insurance starts with measuring it where it actually happens.

- Partner with an InsurTech software vendor for custom solutions. Most carriers cannot build all of this in-house fast enough, and off-the-shelf tools rarely fit complex products or legacy systems. A specialist partner is often the fastest route to a real customer experience transformation strategy for insurance that bends to your business rather than the reverse.

Fix the touchpoints customers actually judge you on, starting with claims, and measure CX at each stage rather than as one annual score.

Binariks experience in insurance software development

We have spent years building the software that carriers use to run the moments this article keeps coming back to. Our insurance work spans the full journey: claims automation and FNOL optimization, AI-driven underwriting, policy and collision-management platforms, and customer-facing InsurTech apps.

Across those projects the through-line is the same one we have argued for throughout this guide, that the claims experience insurance customers remember is built, not bolted on, and that AI-enabled insurance servicing only works when it is wired into the real workflow rather than demoed on a slide.

Let's get back to our example with AI-powered car insurance app .

- The problem: An EU insurer was stuck with manual, slow car damage assessment. Every claim waited on a human to eyeball the damage, which frustrated policyholders and capped how many claims brokers could handle.

- The solution: Beginning with an R&D phase on their existing claims data, we trained a computer-vision model that identifies the damaged part from a customer's photo, classifies the damage across six types, and estimates repair cost in real time, then built it into a mobile app policyholders use directly.

- The result: Assessments run far faster, minor claims are approved automatically, and the manual-review load (and its cost) drops sharply. The app is now in active use across a wide market, and the customer's post-accident wait shrank from a phone call and a queue to a photo and an answer.

That project is a small picture of the larger pattern: using clean data and the right model to deliver insurance personalization at scale and faster service at the same time, without trading one for the other.

Looking to improve your insurance customer experience? Let's talk .

Binariks builds insurance software across claims, underwriting, and customer-facing apps, and our AI car-insurance project shows the pattern we aim for: faster service and smarter automation wired into the real workflow, not bolted on after.

FAQ

Author

Share