In the insurance industry, the First Notice of Loss (FNOL) marks the critical initial step where policyholders report incidents such as accidents or thefts to their insurers. This moment not only initiates the claims process but also significantly influences customer satisfaction and operational efficiency. Traditionally, FNOL has involved manual data collection and processing, leading to delays and potential inaccuracies.

However, the advent of FNOL automation is transforming this sphere a lot. By integrating automated systems, insurers can streamline data collection, reduce processing times, and minimize errors, thereby enhancing the overall customer experience. Technologies such as AI in FNOL play a pivotal role in this transformation, enabling real-time data analysis and decision-making.

In this article, you will discover:

- The fundamental role of FNOL in insurance claims;

- Challenges associated with traditional FNOL processes;

- Benefits of automating FNOL;

- Core technologies that drive FNOL automation;

- Steps to implement an automated FNOL system;

- A real-world success story of FNOL automation.

Let's start from the very beginning!

What is FNOL, and why is it key in insurance claims?

FNOL is the initial step a policyholder takes to inform their insurer about an incident such as theft, damage, or loss involving a covered asset. It marks the beginning of the claims process — and often defines how quickly and effectively that process unfolds.

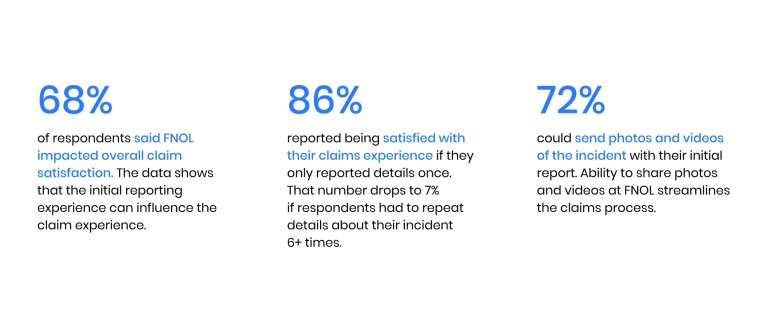

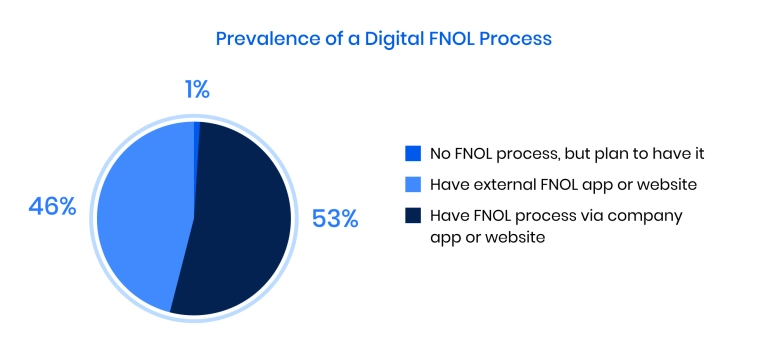

According to the HiMarey survey, FNOL can really make or break the claims experience (Source ):

For insurers, optimizing this stage is more than an operational upgrade — it's a competitive necessity. A slow or error-prone response to an FNOL submission can erode customer trust and increase costs. That's why companies are turning to automated FNOL solutions to streamline intake, reduce human error, and accelerate claims handling.

What makes this transformation urgent is shifting customer behavior. Most policyholders today expect digital-first claims handling and are less likely to stay with providers that don't meet that standard. AI-driven FNOL systems meet this demand by enabling real-time processing, 24/7 responsiveness, and smart triaging based on claim complexity. As part of the broader evolution of AI in the insurance market , these tools are changing how insurers operate — from first contact to final resolution.

Challenges in traditional FNOL processes

Despite its critical role in claims management, FNOL remains one of the most outdated components of the insurance lifecycle. Many providers still rely on manual methods — paper forms, phone calls, siloed systems — that make it hard to keep up with customer expectations or operational demands. This block outlines the key challenges insurers face when working with legacy FNOL workflows and sets the stage for why digital transformation is essential.

At the core, outdated FNOL processes hinder speed, accuracy, and trust. Below are the most persistent issues holding insurers back — and why digital FNOL solutions are becoming non-negotiable:

- Manual reporting

Policyholders are often required to initiate claims through call centers or fill out static online forms. These methods are slow, error-prone, and heavily dependent on human availability — especially problematic during peak hours or after large-scale incidents.

- High response time and processing delays

Once a claim is submitted, it can sit in a queue for hours or days before being reviewed. Without automation, routing to the correct department or triaging by severity becomes a manual, time-consuming task that stalls the entire process.

- Inaccurate or incomplete data from policyholders

Customers may forget key details, submit unclear photos, or provide conflicting information. Without structured input fields or AI-assisted validation, insurers waste time chasing down missing elements — delaying resolution and increasing operational costs.

- Fraudulent claims due to lack of real-time verification

Legacy FNOL systems lack the tools to cross-reference data in real time or detect red flags. This opens the door to inflated or fabricated claims that could be caught early with AI-powered image analysis, metadata checks, or behavioral profiling.

- Poor customer experience due to slow claim initiation

When policyholders face delays just getting a claim acknowledged, it sets a negative tone for the entire experience. In a market where digital-first competitors are raising expectations, weak customer experience in insurance is a liability insurers can't afford.

- Limited scalability during peak events

After natural disasters or large-scale accidents, claim volumes surge. Manual FNOL processes aren't built to handle spikes, resulting in long hold times, processing backlogs, and growing frustration among customers and internal teams.

- Siloed communication between departments

Without centralized platforms, data from FNOL submissions gets fragmented across teams. Adjusters, underwriters, and customer service reps may work from different versions of the truth, causing miscommunication, delays, and inconsistent outcomes.

- Lack of actionable insights

Manual FNOL handling generates vast amounts of unstructured data that typically go unused. Without intelligent automation to analyze trends or flag anomalies, insurers miss valuable opportunities to improve fraud detection, refine underwriting, or tailor services.

While these issues are deeply embedded in legacy systems, change is underway. AI is transforming FNOL by eliminating bottlenecks and bringing intelligent automation into the equation. The result? Faster resolution, more accurate data, and a more loyal customer base — all pointing toward the future of FNOL automation.

Key benefits of automating FNOL

The traditional FNOL process isn't just inefficient — it's a missed opportunity. Every claim reported is a moment to strengthen trust, demonstrate speed, and improve margins. That's why insurers are rapidly adopting AI-driven FNOL automation to modernize this critical entry point in the claims lifecycle.

Here are some stats to back it up from the Claims Performance Benchmarks Report 2023 (Source ):

By replacing manual intake with intelligent, automated workflows, insurers gain both operational agility and strategic advantage. Below are the key benefits that FNOL claims automation delivers:

- Faster claim acknowledgment and triage

Automated systems instantly capture and route FNOL data to the appropriate department, enabling insurers to respond within minutes — not days. This speed reduces pressure on internal teams and reassures customers their case is being handled.

- Greater accuracy and consistency

Structured digital input, real-time data validation, and AI-powered document processing eliminate human error and ensure consistent quality across all submissions.

- Lower operational costs

With fewer manual steps, companies reduce overhead associated with staffing, training, and follow-ups — allowing resources to be reallocated to higher-value tasks like fraud detection and customer retention.

- Improved fraud prevention

AI tools can cross-check claim details, flag suspicious patterns, and assess metadata in real time — helping insurers catch fraudulent submissions early without slowing down legitimate cases.

- Higher customer satisfaction

Customers receive faster, more straightforward responses and gain access to digital self-service tools. In an industry where trust and responsiveness matter, automation enhances every touchpoint.

- Data-driven decision-making

Automated FNOL platforms collect structured, actionable data at scale. This unlocks insights for better risk profiling, loss forecasting, and product refinement — building long-term value.

In short, modernizing FNOL processes isn't just a matter of speeding things up — it's a strategic shift in how insurers interact with policyholders, handle risk, and grow at scale. As more companies embrace intelligent automation, it's quickly becoming a core component of competitive insurance operations.

Embrace InsurTech innovation with custom software development

Core technologies powering FNOL automation

Modernizing claims intake requires more than just digitizing forms — it demands smart, interconnected technologies that turn a manual task into a streamlined, responsive experience. Here's a breakdown of the core components that support an automated FNOL process, making it faster, more innovative, and more secure.

1. Artificial intelligence

AI is the backbone of FNOL automation. It powers real-time data extraction, intelligent triaging, and decision-making based on historical claim patterns. By learning from past outcomes, AI helps assess risk levels, detect inconsistencies, and prioritize claims — all without human input.

2. Machine learning

ML enables systems to improve over time by continuously analyzing new data. It refines claim predictions, adapts fraud detection models, and customizes responses based on previous customer interactions, making the entire FNOL journey more accurate and adaptive.

3. Natural language processing (NLP)

NLP allows platforms to understand and interpret unstructured inputs — such as policyholder messages, emails, or voice transcripts. This tech ensures that even non-standard claim submissions are processed efficiently and routed correctly within the automated FNOL process.

4. Robotic process automation (RPA)

RPA handles repetitive tasks like data entry, document upload, or pulling information from legacy systems. It ensures faster processing, fewer errors, and seamless integration between new and existing software platforms.

5. Image and video analysis

With the increasing use of smartphones in claims reporting, image and video recognition technologies analyze visual evidence submitted by customers. This supports real-time damage assessment, fraud detection, and faster decision-making.

6. Digital customer interfaces

Smart intake forms, mobile apps, and self-service portals guide users step-by-step through claim submission. These tools reduce friction, ensure cleaner data collection, and offer a clear path for automating FNOL in a user-friendly way.

Together, these technologies enable insurers to transition from reactive claims processing to proactive service delivery. The result? A smoother, faster, and more transparent experience for both insurers and their policyholders.

According to InsurTech Digital, top platforms already integrate these technologies at scale (Source ). For example:

- Snapsheet uses AI and digital intake tools to manage claims efficiently across mobile channels, reducing processing times and manual effort.

- EIS's ClaimCore platform combines RPA and data analytics to automate complex claims workflows, helping insurers reduce costs and respond faster to high-volume events.

- Insurity leverages AI for fraud detection and claims triage, allowing insurers to flag high-risk submissions early and streamline low-risk cases — showcasing how tech-driven solutions are shaping the next phase of automation.

Steps to implement an automated FNOL system

Shifting from manual to digital FNOL is a complex transformation that touches workflows, people, and infrastructure. Insurers often underestimate the implementation phase, which leads to missed deadlines, budget creep, and underwhelming results. Below are the key challenges insurers face when deploying first notice of loss automation, along with insights from Binariks on how to handle each one.

1. Assessing current processes and identifying weak spots

Most insurers operate with heavily fragmented FNOL processes: multiple intake channels, outdated forms, inconsistent handoffs, and undocumented decision-making paths. These inefficiencies aren't always visible until implementation is already underway — when it's too late to fix them cleanly.

What we recommend: Don't start with tools — start with clarity. Map out every touchpoint in your FNOL journey, from the moment a policyholder reports an incident to when the claim is handed off for adjustment. Interview both frontline staff and customers. Look for repeated friction points like back-and-forth emails, long handoffs, or unclear routing logic. This baseline will drive smarter decisions when selecting automation features and scope.

2. Choosing the right technologies and vendors

The wrong tech stack can cost more than money — it can lock you into rigid workflows, introduce data silos, or require costly rework when scaling. Vendors often oversell features that sound great on paper but don't address your specific FNOL needs.

What we recommend: Focus on flexibility and industry alignment. Choose platforms that offer modular capabilities, easy API integration, and support for insurance-specific workflows. Look for vendors with real-world experience in AI-driven solutions for FNOL, not just general process automation. Avoid one-size-fits-all offerings that can't adapt as your operation evolves.

3. Integrating with existing systems

FNOL touches nearly every part of the insurance ecosystem — CRM for customer data, ERP for billing, claims management for workflow, and documentation. Integration across these systems is critical but often underestimated in terms of complexity and hidden costs.

What we recommend: Build a cross-functional integration plan early. Don't rely on manual middleware fixes or point-to-point connections that won't scale. Use robust data mapping strategies and RESTful APIs wherever possible. Our engineering teams often recommend setting up a shared service layer that allows new automation to plug in without disturbing legacy systems — this creates flexibility for future upgrades.

4. Testing and training internal teams

Even the best-designed automation can fail if internal teams don't trust it, understand it, or know how to use it. Many FNOL rollouts fail because they skip usability testing or treat training as an afterthought. That leads to delays, frustration, and in some cases — total abandonment of the new system.

What we recommend: Run internal pilots and stress-test workflows with actual user data. Start with a small, high-volume line of business (like auto or property) and collect feedback before full deployment. Train each team based on how they'll interact with the new FNOL system — not just generic "platform training." Encourage ownership by involving key users early in the rollout.

5. Monitoring performance and continuous optimization

Too many insurers treat automation like a fixed investment instead of an evolving capability. Without active monitoring, even well-built systems drift from business goals, fail to adapt to new regulations or deliver a degraded experience over time.

What we recommend: Set performance metrics from day one — not just claims processed, but response times, error rates, drop-offs, and customer satisfaction. Use that data to build dashboards for both operational teams and leadership. Schedule monthly reviews in the first quarter post-launch, then quarterly thereafter. Treat optimization as part of the job — not a side project.

Implementing first notice of loss automation is a strategic move that pays off when done right — but it's not plug-and-play. By addressing these challenges head-on and working with partners experienced in AI-driven solutions, insurers can reduce risk, speed up rollout, and create systems that scale with the business.

Success story of FNOL automation

To show how FNOL automation works, here's a real-world example of how we helped a global insurance provider modernize and stabilize its claims intake system.

Binariks partnered with a global private insurance provider to enhance and stabilize its critical FNOL process . The client — a major player in the property and casualty space with $45–50 billion in annual turnover — faced growing pressure to modernize its claims intake and Loss Data Capturing systems.

Fragmented integrations, limited scalability, and recurring service disruptions were slowing claim registrations and inflating operational costs.

Our team was brought in to solve a layered challenge: ensure uninterrupted system performance, enable seamless integration with the Claim Management System (CMS), and unlock capacity for innovation.

We assembled a dedicated team of five developers, an AQA engineer, a business analyst, and an architect who quickly immersed themselves in the client's architecture. Here is how our team approached the project:

- Designed and implemented a secure middleware layer between FNOL and CMS;

- Developed backend services for structured claim registration, search, and updates;

- Automated infrastructure provisioning using AWS-CDK;

- Ensured secure data handling with OAuth2, IAM, and Vault;

- Migrated CI/CD workflows from Bamboo to GitHub Actions;

- Introduced monitoring and logging via AWS CloudWatch, Datadog, and Splunk.

Optimizing FNOL for an insurance provider

Explore how we ensured seamless data flow, improved service stability, and cut operational costs.

The results didn't keep us waiting. Claims now move through a stable, scalable architecture with minimal downtime. The client cut costs by reducing manual handling, reallocated internal resources to strategic work, and gained a foundation ready for future development.

Beyond solving technical debt, the project deepened our expertise in insurance automation and positioned Binariks as a long-term technology partner for high-stakes, high-scale transformation in insurance.

Conclusion

Modernizing the FNOL process is no longer optional for insurers aiming to stay competitive. Legacy claims intake systems are slow, error-prone, and costly and often fall short of what customers expect.

By implementing AI, intelligent automation, and scalable cloud infrastructure, insurers can dramatically improve claim speed, accuracy, and service quality. From faster triage to real-time fraud detection, the benefits of automation reach across the entire claims lifecycle.

But success doesn't come from tools alone — it requires the right architecture, a clear strategy, and expert execution. That's where Binariks brings value. We've helped global insurers build secure, scalable, and future-ready FNOL systems that cut costs and improve operations. If you're ready to elevate your claims platform, explore our insurtech development services , and let's build a solution that actually delivers.

Author

Share