Managing General Agents (MGAs), insurance agents with underwriting authority, represent an enormous opportunity for the insurance industry. By the nature of their work, MGAs push forward innovation and technology that goes beyond them and spills into more traditional insurance instruments. Why? Because MGAs are built to move fast.

Unlike traditional carriers, they aren't slowed down by legacy systems or rigid processes. They're incentivized to launch products quickly, serve niche markets, and differentiate through technology—so innovation isn't optional; it's essential to their survival and growth.

The investment into MGAs has been rapidly growing over the last couple of years, mirrored by the growth of embedded insurance , automation, and AI, all of which are the instruments in MGAs work. There is a growing need among businesses to understand how this new disruptive force in insurance is operating.

In this article, we outline the role of MGAs, list the differences between an insurance broker and an MGA, and explain the technologies and distribution models they use. Learn how Binariks can support your digital transformation with MGAs.

What is an MGA? Role and origins in modern insurance

A Managing General Agent (MGA) is an insurance intermediary with delegated authority from insurance carriers. This authority enables MGAs to perform key functions such as underwriting , setting pricing, issuing policies, and—in specialized or underserved markets like cyber insurance, pet insurance, or gig economy coverage—managing claims process or developing custom-tailored products.

The relationship with MGAs is initiated by insurance companies looking to enter niche markets or expand distribution without building new internal teams or infrastructure. The access to niche markets allows them to have access to specific customer segments. They can even offer professional liability insurance for small risks. MGAs operate on the insurer's behalf under formal agreements defining their authority scope.

MGAs rose to prominence as a solution to structural inefficiencies in traditional insurance. Carriers were often too large, slow, and reliant on legacy systems to serve fast-evolving markets. The Managing General Agency (MGA) filled that gap. They offer insurers a way to enter new verticals without building internal infrastructure or niche expertise.

In the digital age, MGAs have become the most agile players in insurance—using data, tech, and tailored distribution models to disrupt conventional processes.

What are MGAs and brokers? Key differences explained

The key difference between managing general agents vs. brokers is that MGAs can underwrite and manage insurance policies on behalf of carriers; brokers cannot.

MGAs (Managing General Agents) are insurance intermediaries with underwriting authority granted by insurers. They can price, bind, and manage policies—sometimes even handle claims. MGAs represent the insurance company in this relationship.

Brokers act as intermediaries between clients and insurers but do not have the authority to underwrite or issue policies; they help clients select the policy that best suits their needs from the broad selection of various insurers.

Insurance brokers and MGAs have the same goal—to connect customers with the right insurance coverage—but they serve different sides of the equation. Brokers work for the customer, while MGAs act on behalf of the insurer.

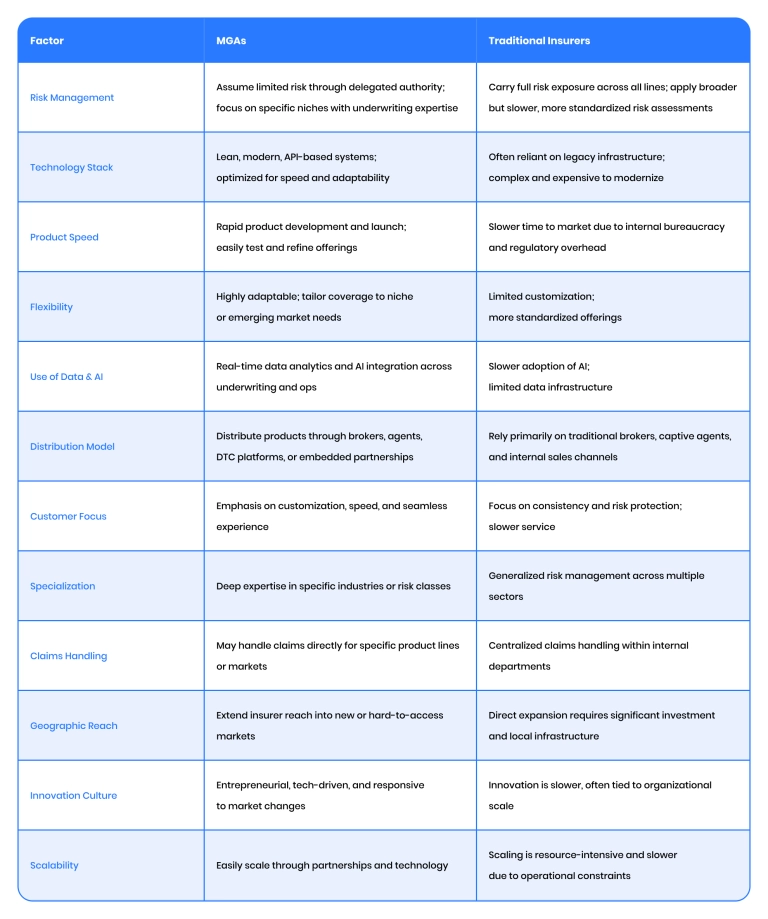

MGAs vs. traditional insurers: A comparative breakdown

Managing general agents (MGAs) strive over traditional insurers in several specific ways. They have enhanced expertise in specific niches, which allows them to structure risks for the insured in a way that transcends the expertise of traditional insurers.

They have access to new technologies without the burden of legacy systems. They also have specific new technologies for specific tasks like claims processing .

This table outlines detailed differences between an insurance broker and an MGA:

When to add a third-party administrator?

Not every MGA handles everything in-house. Some rely on third-party administrators (TPAs) to manage claims and operational tasks. This setup helps them stay lean and scale faster—especially when entering new markets or launching niche products.

In contrast to MGAs or brokers, a TPA (Third-Party Administrator) or third-party broker is an external service provider that handles claims, policy administration, and other back-office tasks on behalf of an insurance company or MGA.

The relationship between a TPA and the insurance company (or MGA) is typically built around efficiency and cost control, with clearly defined responsibilities.

TPAs and MGAs often work together when in-house claims infrastructure isn't practical or available.

TPAs typically handle:

- Claims intake and processing

- Customer service and call center support

- Regulatory reporting and documentation

- Payment coordination and disbursement

You'd bring in a TPA, for example, if your MGA launches cyber insurance for small tech firms but lacks an internal team to handle breach response and forensic coordination. A TPA with cybersecurity claims expertise can manage the entire incident workflow—from initial report to vendor coordination and final settlement—without the MGA building that capacity in-house.

Tech needs of MGAs: Beyond legacy systems

Unlike traditional insurance brokers, MGAs aren't burdened by outdated systems. This lets them use cloud-based, API-driven platforms instead of maintaining outdated legacy systems. Here is a breakdown of the core areas where managing agents prioritize technology:

1. No legacy systems to maintain

Most MGA insurance brokers operate without the burden of inherited infrastructure. This gives them the freedom to adopt lightweight, scalable platforms instead of spending time and resources on maintaining legacy code.

2. Innovation at the core

MGA operations are built around continuous experimentation and rapid iteration. Whether testing new pricing models or launching micro-insurance products, innovation is not a side function—it's central to how they work.

3. API-driven architecture

MGAs work on platforms designed for connectivity. APIs let them exchange data smoothly with carriers, distribution channels, and service providers—enabling real-time underwriting and faster decision-making across the board.

4. Cloud-based infrastructure

Cloud setups let MGAs scale on demand, deploy updates quickly, and support distributed teams. It's a more agile and cost-efficient foundation than maintaining in-house servers.

5. No-code/low-code tools

To stay flexible, many MGA insurance brokers use platforms that let them adjust internal processes without writing code. This speeds up iterations and reduces reliance on dev teams.

6. External data access

Modern MGAs depend on structured external data—such as behavioral signals or location-based risk factors—to improve underwriting precision and offer more relevant products.

7. Automation

Routine operational tasks are often automated to keep overhead low. This includes generating documents, sending reminders, and meeting compliance deadlines.

Embrace InsurTech innovation with custom software development

MGAs' diverse models: Brokers, DTC, and embedded insurance

Modern managing general agents (MGAs) are not tied to a single distribution model. Instead, they thrive by adopting flexible approaches tailored to specific products and markets. Here is how they work with customers:

1. Broker partnerships

It is not always MGA vs broker. Many MGAs collaborate with traditional brokers to expand their reach and tap into established client relationships. In this model, MGAs act as the product and underwriting engine behind the scenes, while brokers handle customer acquisition and servicing.

- Advantage: Combines MGA speed and specialization with brokers’ market access.

- Best for: MGAs entering regulated or relationship-driven markets where brokers maintain strong trust—such as commercial property, construction, or marine insurance.

Example: An MGA offering E&O coverage for law firms partners with a national broker network to access small legal practices across multiple states.

2. Direct-to-consumer (DTC)

Some MGAs go fully digital and market their products directly to end users via intuitive online platforms. These tech-first MGAs streamline the entire insurance journey without intermediaries.

- Advantage: Full control over customer experience, faster feedback loops, and stronger brand positioning.

- Best for: Simple, high-volume personal lines like renters, travel, or pet insurance.

Example: A pet insurance MGA offers a mobile-first platform for fast, self-service coverage.

3. Embedded Insurance

The most innovative MGAs embedded insurance products into non-insurance platforms—like e-commerce sites, travel booking apps, or fintech services. For example, travel insurance is offered at checkout, and pet insurance is bundled with a veterinary app.

- Advantage: Seamless integration into the customer journey leads to higher conversion rates and broader reach.

- Best for: When insurance complements an existing product or service and can be offered contextually.

Example: A cyber insurance MGA embeds coverage into a small business website builder.

MGAs often apply these distribution models to serve risky or hard-to-place businesses. Here’s where each model tends to fit best:

- Cannabis-related businesses – broker-led, given the regulatory hurdles

- Professional liability for smaller deals – often embedded or broker-distributed

- Drone liability for commercial operators – works well as DTC or embedded

- Short-term rental coverage (e.g., Airbnb hosts) – best offered DTC or embedded in booking platforms

- E-sports and gaming event insurance – typically broker-driven for event-level customization

- On-demand gig economy coverage (e.g., delivery and ride-hailing platforms) – fits DTC or platform-embedded distribution

- Digital asset protection (e.g., crypto wallets and NFT theft) – ideal for embedded or direct platforms

- Parametric weather insurance for small farms or outdoor events – often sold DTC or through niche brokers

- Climate-exposed properties in wildfire or flood-prone areas – usually broker-led due to underwriting complexity

Unlocking growth: AI, automation, and data in MGAs

Technologies are at the core of MGAs - they aren't just tools but strategic growth drivers. Here is the context in which AI, Automation, and data are leveraged:

1. Artificial intelligence: Smarter risk selection & personalized pricing

MGAs increasingly rely on AI and machine learning models to handle complex underwriting tasks that were once manual and time-consuming. For example:

- Risk-scoring models analyze diverse data sources like geolocation, weather patterns, IoT device inputs , and customer behavior to assess individual risk profiles.

- Dynamic pricing algorithms allow MGAs to adjust premiums in real time based on market conditions, user behavior, or changes in risk exposure—ideal for usage-based or event-triggered products.

- Through behavioral pattern analysis and real-time anomaly detection, fraud detection AI helps flag anomalies during quote, binding, or claim stages.

Example: A managing general agency (MGA) offering cyber insurance might use AI to scan a company's digital infrastructure and assign a risk score instantly—pricing the policy within seconds, without human intervention.

2. Automation: Scaling operations without scaling costs

Automation allows managing agencies to scale rapidly without bloating their operations teams. Here's where automation shows its strength:

- Quote-to-bind automation enables end-to-end policy creation without manual oversight—ideal for embedded or DTC channels.

- Claims triage bots classify and route claims based on severity and policy terms, often with NLP to read claim descriptions or documents.

- Regulatory and compliance automation helps MGAs stay updated with filing and reporting requirements across multiple jurisdictions automatically.

Example: A pet insurance MGA might automate onboarding and low-value claims, cutting processing time from days to minutes.

3. Data analytics: Fueling innovation and distribution precision

Data is the engine powering managing general agents (MGAs) agility. Rather than relying solely on historical insurer data, MGAs actively gather and process their own streams of real-time data, such as:

- Customer behavior analytics : Track quote abandonment rates, compare demographic data, and adjust UX or coverage based on conversion patterns.

- Loss trend analysis: Use predictive modeling to adjust underwriting strategy in response to claim trends before they spike.

- Channel performance metrics: Identify the most effective distribution channels (e.g., embedded partner A vs. broker B) and optimize acquisition spending accordingly.

Example: A managing agency focused on gig economy coverage might identify a growing concentration of food delivery workers in a metro area and launch a tailored product for that audience using targeted digital ads.

How Binariks empowers MGAs with tech expertise

In 2025, the MGA sector will likely see heightened competition for tech and coding talent, with a focus on roles that support digital transformation and innovation.

Offering MGAs the resources and support to build teams capable of driving industry-leading results is essential.

Even with modern systems, an insurance broker faces real challenges. APIs don't always play well with legacy partners, cloud platforms raise compliance questions in regulated markets, and automation or no-code tools can hit limits when products get more complex. Accessing clean, reliable external data at scale is another ongoing hurdle. This is when a dedicated IT partner for MGA insurance brokers can step up.

At Binariks, we know MGAs succeed when they can move fast and stay flexible. Our team provides insurtech development services tailored to help them do just that—whether it's building cloud-native platforms, integrating AI into underwriting, or improving the insurance customer experience . We also support MGAs with advanced business intelligence in insurance, helping them use data better to stay competitive in the evolving AI insurtech market. Here is what we can do:

- Designing and building custom underwriting platforms that scale with product complexity

- Implementing API-driven policy issuance and claims workflows, even when partners run on older infrastructure

- Integrating AI/ML tools for dynamic pricing and fraud detection—without sacrificing explainability

- Using real-time analytics and business intelligence in insurance to improve decisions across underwriting and distribution.

Author

Share