How to use AI in the insurance industry? In 2026, artificial intelligence continues to revolutionize every industry it comes in contact with. In insurance, its value lies in improving risk assessment accuracy, increasing customer satisfaction , and streamlining claims processing.

In this article, we explore the continuous impact of AI in the insurance industry, while focusing on the real AI use cases in insurance, from claims processing to agentic AI and data-driven insights, and the regulatory landscape surrounding it all.

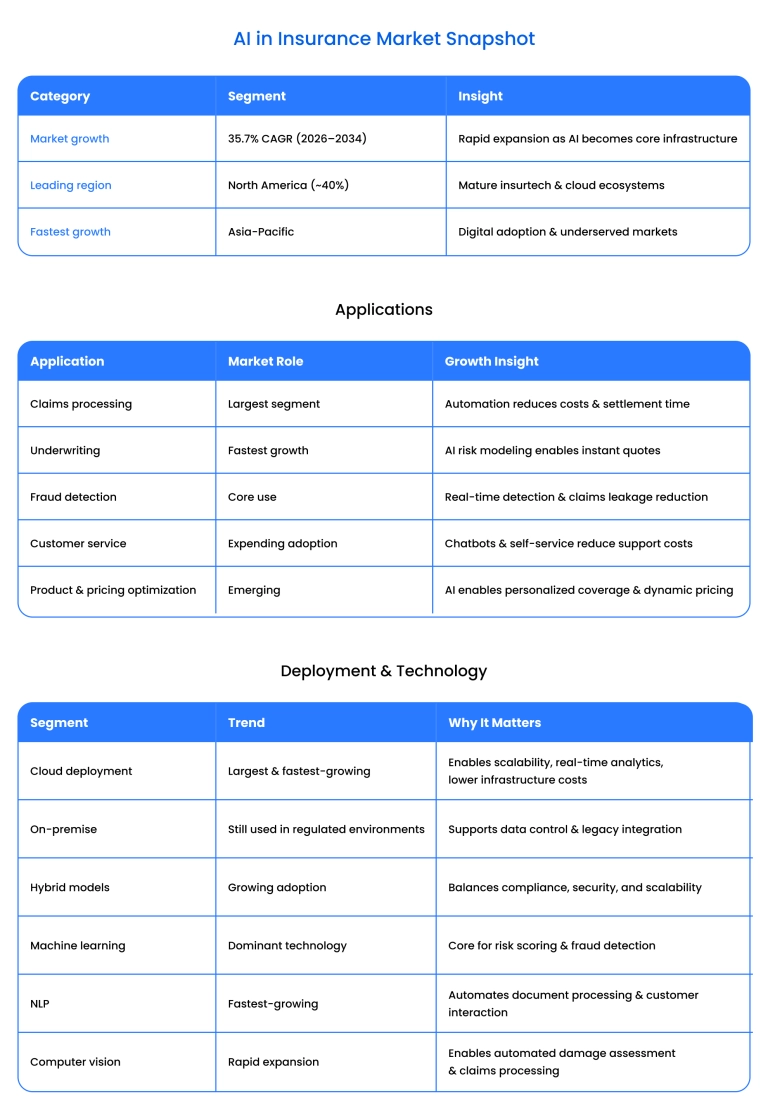

AI in the insurance market size: Key facts and stats

Here is the brief state of AI in insurance market analysis:

- The market is forecast to reach over USD150 billion by 2034, growing at ~35% CAGR, reflecting rapid enterprise adoption.

- 80% of insurers are actively deploying AI in at least one core function as of 2026, marking a shift from pilots to scaled production use.

- The main driver of market growth is the growing need to automate claims processing as claim volumes continue to increase.

- Region-wise, North America leads the AI in the insurance market with a 40 % share. The region adopts advanced analytics quickly and benefits from large-scale investments. Asia-Pacific is the fastest-growing region, driven by the expansion of digital insurance and government-backed AI initiatives. Europe is now accelerating adoption due to regulatory modernization. Emerging markets in Latin America, Southeast Asia, and the Middle East are also investing in AI applications in insurance.

Benefits of AI adoption for insurance

The benefits of AI in insurance include cheaper, more efficient, and more customer-friendly services. Here is the longlist:

- Improved risk assessment: AI algorithms can analyze vast amounts of data, including non-traditional sources, to assess risks (telematics, behavioral, and environmental inputs). You can train AI for insurance on your demographic data. The adoption of artificial intelligence in insurance leads to more effective pricing models and underwriting processes. Also, they help detect fraud.

- Enhanced customer experience : AI-driven chatbots and virtual assistants provide 24/7 customer support. Personalized AI recommendations can also tailor insurance products to individual customer needs.

- Efficient claims processing: AI in insurance can automate and streamline the claims processing workflow . This reduces manual intervention and speeds up claim resolution. The result is a cheaper process and higher customer satisfaction.

- Fraud detection and prevention: AI and ML in the insurance industry can detect patterns and anomalies that may indicate fraudulent activity. They analyze historical data faster than any other current method.

- Operational efficiency: AI in the insurance industry enables automation and optimization across various processes. As a result, it reduces costs and frees up human resources for more complex tasks.

- Data-driven insights: AI can process and analyze large datasets to provide actionable insights. This helps with strategic decision-making and new market opportunities.

- Personalized marketing and customer retention: Marketing is, in fact, a critical application of artificial intelligence in insurance. AI enables more targeted, personalized marketing campaigns by leveraging better customer data. This improves retention rates.

- Predictive risk prevention: By analyzing data, AI helps insurers identify and mitigate risks before losses occur.

- Regulatory compliance & audit readiness: AI in insurance supports compliance monitoring and documentation.

Will adopting GenAI mark the next chapter for your business?

Download our free whitepaper now to find out.

Top AI use cases for insurance

Let's look into some real-life examples of how artificial intelligence in the insurance industry is used:

1. Claims processing

We're seeing a major shift in claims handling. Automation is now handling the grunt work of extracting data, triaging files, and speeding up settlements so adjusters can focus on complex cases.

Computer vision models can detect and classify damage from photos, while NLP extracts claim details from documents. Insurers use confidence scoring to automatically approve straightforward claims while adjusters keep working on more complex cases. Lemonade's instant claims model and Tractable's computer vision platform are well-known examples of automation-first claims handling.

Binariks implemented this approach for a car insurance provider by building a mobile solution that detects six types of vehicle damage (including dents, cracks, and glass damage), associates them with specific car parts, and estimates repair costs in real time.

We designed an AI-driven mobile workflow that combines computer vision damage detection for the goal. As a result of this adjustment, minor claims can now be approved automatically. The solution significantly reduced manual reviews, improved assessment accuracy, shortened claim turnaround times, and increased customer satisfaction.

Another example is FNOL workflows optimization that involved a global P&C insurer that needed to improve First Notice of Loss (FNOL) processing and post-claim data flow. Binariks optimized FNOL workflows by building secure middleware services that unified loss data from multiple intake channels and integrated it directly with the claims management system.

2. Fraud detection

Fraud detection systems use machine learning and network analytics to identify suspicious patterns in claims histories and billing behavior.

Modern solutions are even capable of detecting complex, organized fraud rings, and not isolated incidents. AI-driven fraud detection can reduce claims leakage by 30–50% and identify suspicious claims in real time.

Platforms such as FRISS, Shift Technology, and SAS are examples of solutions that provide continuous fraud monitoring and risk scoring. Fraud detection models help insurers intervene earlier and improve investigation efficiency while avoiding financial losses.

3. Underwriting

Underwriting is one of the highest-value areas for AI because it turns messy inputs into structured risk decisions. AI is used to classify submissions, extract critical fields from broker-provided documents, enrich data from internal/external sources, and support faster quote turnaround.

Many insurers use predictive models to forecast loss probability and severity. Some of the new GenAI patterns help summarise submissions and surface key risks for underwriter review.

Some famous examples of AI use cases in insurance for underwriting are Earnix for pricing and underwriting analytics, and Zest AI for automated risk modelling.

At Binariks, we implemented AI-based insurance underwriting transformation at scale by converting highly variable broker submissions into standardized data for a leading insurance company in the US and UK markets.

As a result, the company achieved real-time data processing, with 80%+ automation of manual data extraction and validation. Some of the less expected, but excellent, benefits included improvements in data quality and compliance. The company also used the new infrastructure as a template for rapid deployment across other business units.

4. Customer experience

AI improves the customer experience by reducing friction in the most stressful moments of the customer journey, such as filing a claim after an accident or health event or selecting the right coverage. Chatbots can handle routine questions and guide customers through self-service steps, while personalization models recommend coverage options or next-best actions based on each customer's unique context.

Insurtech companies like Lemonade and Insurify are well-known for pioneering AI-enabled customer interactions.

The best customer experience outcomes occur when platforms connect conversational interfaces to real workflows (policy updates, claim status, document intake), rather than investing in chatbots as standalone “FAQ machines” without regard for context.

5. Agentic AI

Agentic AI refers to AI systems that can independently plan and carry out multi-step tasks by coordinating data, tools, and workflows to complete a business process from start to finish.

In insurance, it is used in document-heavy work such as claims analysis and legal reviews. Agentic AI combines orchestration frameworks with retrieval-augmented generation (RAG), evaluation/observability, and human-in-the-loop fallbacks for high-risk decisions.

At Binariks, we built an AI-powered, agent-based claims analysis pipeline for a global commercial insurance provider with 50,000 employees and a USD 50 billion annual turnover, which was drowning in an enormous volume of annual workflows. This resulted in a 90% reduction in the time required to extract and analyze risk-related data from documents and 80-90% fewer manual review cycles.

A related agentic pattern is contract validation, where the system cross-checks contracts against business and compliance rules and generates traceable validation reports. Binariks helped achieve an 80% reduction in average contract review time and a 30% increase in underwriter productivity through AI-powered contract validation . The company scaled 10,000+ contracts per month via a cloud-native architecture and achieved USD1.5 million in annual savings.

6. Automated document intake & processing

Insurers receive submissions and claim-related documents in inconsistent formats.

AI in insurance software is then used to classify documents and improve the data quality. A common pattern is confidence scoring: high-confidence extractions go straight through, while low-confidence cases are routed for review.

Binariks implemented this approach in a high-volume intake workflow in which documents arriving by email were parsed into structured system entries, and uncertain cases were routed for quick verification for a global provider of risk-management systems .

7. Policy review and management

AI in the insurance industry is also used for policy changes and renewals.

NLP can interpret customer intent and extract the required information from messages. Predictive models can also identify customers at risk of non-renewal and proactively reach out to them. This use case becomes significantly more valuable when integrated with core policy systems and when insurers maintain strong governance around what the AI can change automatically vs. what requires approval.

Planck and PolicyGenius are two platforms that utilize AI to help insurers manage policies (personalize policies, ensure regulatory compliance, and handle policy administration tasks).

8. Dynamic pricing optimization

AI is used to improve pricing accuracy by modelling loss probability and adapting prices based on portfolio performance.

In auto insurance, telematics-based pricing is the best-known example of this strategy. Metromile offers pay-per-mile auto insurance, with premiums based on actual driving distance and telematics data. Many insurers apply machine learning to continuously test rate impacts.

9. Risk engineering

AI enables insurers to shift from reactive loss coverage to proactive risk mitigation. There are many ways to detect risk, including IoT sensors and telematics data.

In property insurance, aerial imagery and geospatial data can identify flood risk or even simple roof deterioration. Cape Analytics is the company widely cited for property intelligence derived from imagery and geospatial analysis. Octo Telematics uses AI to maintain insured assets through IoT devices installed in vehicles.

10. Regulatory compliance

Regulatory complexity continues to increase across insurance markets, and AI helps insurers maintain compliance by monitoring workflows and tracking regulatory updates. AI systems can automatically flag deviations from regulatory requirements and maintain traceable audit logs.

Insurance companies using AI, like Ascent, monitor regulatory changes and map them to internal controls with its help.

11. Coverage personalization

AI helps customers choose coverage options by analyzing their demographics, risk profiles, and behavioral data. Platforms like Policygenius use AI to recommend health insurance plans by comparing different options and highlighting the best fit for the customer's needs.

Factors that might be included are medical history and current health status. Personalization is known to improve conversion rates and customer satisfaction.

12. Data-driven insights

AI solutions in insurance help insurers understand profitability drivers and customer behavior trends .

For example, an insurer may discover through AI portfolio analysis that drivers in a specific urban area generate higher claim frequency due to theft rates. The insurer can refine pricing for that segment or adjust underwriting guidelines for that area, or even introduce theft-prevention incentives. This is very convenient because they don't have to raise rates across the entire portfolio.

Solutions such as Cape Analytics and Atidot offer advanced analytics for strategic planning. The insights help insurers identify underserved segments and improve the long-term performance of portfolios.

If you feel like the AI and insurance solutions covered in this article are not what you're looking for or are not enough to adequately respond to the unique needs of your business, you can create custom AI /ML solutions with an experienced team like Binariks .

AI regulation in insurance: From NAIC to global frameworks

The insurance industry is heavily regulated, and the adoption of AI introduces an additional regulatory layer. Here is how AI regulations in the insurance industry work in the US, in Europe, and globally:

United States: NAIC-led expectations + state-by-state enforcement

In the US, AI oversight in insurance is principles-based and enforced at the state level.

The NAIC Model Bulletin: “Use of Artificial Intelligence Systems by Insurers” serves as the most widely referenced baseline. The bulletin is not a law; it is guidance issued by the National Association of Insurance Commissioners (NAIC) to help state regulators supervise insurers’ use of AI within existing insurance laws.

It becomes a law when a state insurance department adopts it either formally by issuing its own bulletin based on the model or informally by incorporating its expectations into regulatory supervision. As of 2026, states like Colorado, New York, and California have issued AI bulletins aligned with the NAIC framework.

AI oversight in US insurance is enforced by state regulators, who use their existing supervisory authority to enforce it. Aside from the bulletin, they consider existing consumer protection laws, as well as privacy and data protection laws such as the Gramm-Leach-Bliley Act (GLBA) and the California Consumer Privacy Act (CCPA).

The bulletin clarifies expectations for insurers using AI across underwriting, pricing, claims, fraud detection, and customer service.

For instance, transparency in NAIC means that insurers must be able to explain how AI contributes to decisions, with documentation describing the model's purpose and decision logic, and the ability to explain decision factors to regulators. Where required, they must also provide consumer-facing explanations. For example, if a claim is denied, the insurer must clearly explain why.

Europe: EU AI Act + insurance-sector governance + resilience rules

In Europe, the regulatory picture is more centralized. The EU AI Act (Regulation (EU) 2024/1689) establishes a cross-industry standard framework for AI regulation. This act classifies high-risk AI systems, gives companies requirements to put governance and risk controls in place, and gives national regulators the authority to investigate violations and issue fines.

The Act was published in the Official Journal on July 12, 2024, and entered into force on August 1, 2024, with a staged application.

For insurance specifically, EU oversight is also shaped by sector rules and supervisory guidance. In August 2025, EIOPA published an Opinion for national supervisors clarifying how existing insurance legislation’s governance and risk-management expectations apply to AI systems, using a risk-based, proportionate approach.

Alongside AI governance, insurers must comply with DORA, which took effect on January 17, 2025, and requires financial entities to strengthen ICT risk management and third-party vendor oversight.

Globally, no one standard fits all legal acts, but some of the following are considered recommendations in many different countries:

- The International Association of Insurance Supervisors promotes responsible AI use aligned with consumer protection and risk management.

- The Organization for Economic Co-operation and Development AI Principles provide widely adopted guidance on trustworthy AI.

- International Organization for Standardization standards, such as ISO/IEC 23894, support AI risk management and governance practices in different countries.

- The evolving legislation in both the US and the EU will affect subsequent acts adopted in different countries.

Embrace InsurTech innovation with custom software development

AI adoption challenges in insurance

AI for insurance companies is now an unparalleled way of making experiences faster and easier. However, some significant limitations remain, as AI can't work for everything. Moreover, there are significant roadblocks in the development process.

One of the most visible risks is model accuracy and bias. Generative AI systems can produce incorrect outputs (“hallucinations”) and may inherit biases from their training data, especially when trained on broad internet sources. This raises fairness and discrimination risks.

Regulatory bodies such as the National Association of Insurance Commissioners emphasize that insurers remain responsible for ensuring that AI systems do not result in unfair discrimination and must implement testing and monitoring controls. Research from McKinsey & Company highlights that bias and model reliability remain top concerns in AI adoption across financial services.

AI also has limitations in complex risk evaluation, particularly in life and health insurance. Underwriting decisions in these areas involve nuanced medical histories and substantial contextual judgment. Industry analysis emphasizes hybrid decision models that combine AI insights with human oversight to improve accuracy and fairness.

McKinsey argues that while AI can automate 70% of routine tasks, it cannot replace "high-value decision-making." They explicitly state that, for complex risks, the goal is "Augmented Underwriting," in which AI handles data processing while humans handle the rest.

Insurance analytics and AI require high-quality, accurate data to function effectively. Insurers often struggle with legacy systems and siloed data, making it challenging to access and integrate data across departments. That is where proficiently crafted AI solutions for insurance , such as those developed by experts like Binariks, can prove invaluable.

There is often a gap in the workforce's skills to manage AI solutions. Training current employees and recruiting new talent with AI expertise is challenging for many insurers. Gartner identifies the "talent shortage" as one of the top barriers to digital transformation in the financial sector, noting that internal upskilling often lags behind technological change.

AI and insurance trends through 2030

Through 2030, insurers are expected to move beyond pilot projects and embed AI into core operations.

One of the most significant AI in insurance market trends is the expansion of natural language processing (NLP) across the insurance value chain. NLP is already powering conversational assistants and customer service automation, but its role is expanding into document intelligence, claims intake, regulatory compliance, and medical/legal review. Sentiment analysis is also gaining traction, allowing insurers to prioritize urgent cases.

Generative AI is emerging as a transformative force, enabling insurers to automate communication, summarize complex documents, generate policy explanations, and support underwriting and compliance workflows. Generative AI supports decision-making by synthesizing large volumes of structured and unstructured data into explainable insights. By 2030, generative AI is expected to play a major role in agentic workflows .

At the core of risk management, predictive modelling continues to evolve. Insurers are expanding beyond traditional actuarial models toward real-time risk forecasting using telematics, IoT data, behavioral signals, and environmental data. Predictive analytics enables dynamic pricing, early claim severity estimation, churn prediction, and proactive loss prevention. This shift supports a transition from reactive coverage to preventive risk management.

Machine learning and advanced analytics are enabling insurers to process diverse datasets at scale, from geospatial imagery to behavioral and transactional data. These capabilities support improved underwriting accuracy and fraud detection.

Automation will continue to expand through robotic process automation (RPA) and intelligent workflow orchestration. While RPA began as a tool for automating repetitive tasks, it is increasingly integrated with AI to enable end-to-end process automation. Insurers use these technologies to streamline policy administration, claims handling, compliance checks, and document processing.

In property and auto insurance, image recognition and computer vision are improving damage assessment and risk evaluation. AI models can analyze photos to estimate repair costs, detect structural risks, and assess property conditions. Combined with aerial imagery and geospatial data, computer vision is enabling more accurate risk assessment and proactive risk mitigation.

Finally, insurers are moving toward AI-native operating models supported by cloud infrastructure and data platforms. This shift enables real-time decision-making, continuous model improvement, and enterprise-wide analytics. As regulatory expectations evolve and customer expectations rise, insurers that integrate AI responsibly and transparently will be best positioned to compete in a more digital, predictive, and personalized insurance landscape.

By 2030, AI may not replace human expertise in insurance, but will surely augment it, enabling faster decisions and better risk management across the entire insurance lifecycle.

Modernize insurance. Lead with innovation

Explore how to overcome the most pressing industry challenges with advanced technology – starting now

Final thoughts

Artificial intelligence is becoming the operational backbone of the industry; it is no longer just an experimental tool.

There is a growing integration of AI tools across various aspects of insurance, from claims processing to fraud detection . Throughout the next years, we will see more risk and balancing of opportunities for AI in the insurance industry. Physical robotics, open-source data, and IoT will further enhance the existing AI architecture in insurance.

All of this means 2026 is the time to leverage the power of AI and choose which technologies will best benefit their company and customers. If you are an insurer, start prioritizing data infrastructure before AI models. No AI can outperform the data on which it is based.

If you are an investor, invest in data infrastructure and insurance-specific platforms rather than general-purpose AI tools. For regulators, it is time to coordinate across jurisdictions to reduce fragmentation. Balancing innovation with consumer protection remains a critical task. Technology partners should build explainability and governance into their core product.

Whatever your role in the insurance industry is, Binariks is here to help develop and train AI models and integrate AI with your existing systems.

Author

Share