In the insurance industry, data has always been a driver. However, big data now serves as a disruptive force, completely revolutionizing how data is handled and interpreted. What is more, big data in insurance risk assessment creates a competitive advantage, and businesses are eager to reap the financial benefits of big data involvement.

As an insurance business, to venture into risk assessment with big data, you need to weigh in all benefits and risks and make an informed decision. With a successful strategy in place, you can enjoy big data benefits for risk assessment, including better segmentation of the customer base, improved underwriting and fraud detection strategies, and many more.

In this article, we highlight the benefits, the challenges, the use cases, and the best practices of integrating big data into risk analytics.

How big data can improve risk assessment in insurance

In addition to other benefits of AI in insurance , big data benefits for risk assessment are irreplaceable. Big data offers insights into vast information on customer demographics, credit, and claims history. Big data helps analyze clients to predict the occurrence of specific risks.

Let's look into interactions between data analytics and risk assessment in more detail. Big data can significantly enhance risk assessment in the insurance industry through various approaches:

Identification and segmentation of risks

Big data allows insurance companies to gain deeper insights into risk factors affecting different customer groups. By analyzing large volumes of data from various sources such as social media, IoT devices, and public records, insurers can recognize patterns in customer behavior, environmental conditions, and historical claims data to predict potential risks.

Big data analytics for risk and insurance also allows for the segmentation of customers. You can classify customers into risk categories based on their behaviors and demographics. It is also possible to search for entirely new customer segments.

Pricing and underwriting

Big data enables more precise pricing and underwriting decisions by providing precise information that can be used to create dynamic pricing. You can adjust insurance premiums in real-time by continuously monitoring risk factors such as driving habits, health metrics, and other risk-related data.

Risk assessment with big data also means enhanced underwriting. You can utilize predictive analytics to assess the likelihood of claims and set more accurate underwriting criteria, reducing the possibility of underwriting losses.

Fraud detection

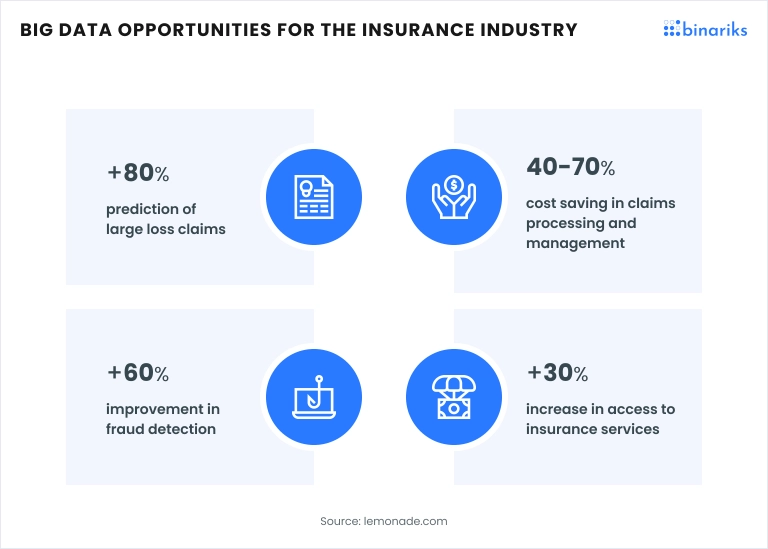

One of the most significant benefits of big data is its ability to detect and prevent fraudulent activities through anomaly detection and cross-referencing data. Big data for insurance risk assessment enables anomaly detection using machine learning algorithms to identify unusual patterns in claims data that may indicate fraud. Cross-referencing data is made possible by comparing claims data with external databases to spot inconsistencies and verify the authenticity of claims. Successful fraud detection through big data risk assessment helps reduce losses by preventing fraudulent claims.

Claims management

Big data improves the efficiency of claims management processes, reducing costs and improving customer satisfaction through automated processing and predictive analytics.

With automated processing, you can implement automated systems that process claims quickly by analyzing data from various sources to verify and validate claims.

Predictive modeling in insurance allows for estimating the likelihood of claim approval and settlement amounts. This leads to faster decision-making and resource allocation.

Customer experience

Beyond risk assessment, big data can enhance overall customer experience with personalized services that better reflect individual customer profiles. Big data analytics in risk assessment helps to offer tailored insurance products and services based on individual customer data. It also helps identify potential issues and reach out to customers before they file a claim.

Examples of how insurance companies use big data

Big data is transforming the insurance industry by enabling more accurate risk assessment, personalized customer experiences, efficient claims processing, and proactive risk management. Here is how famous companies use it in their unique ways:

1. Progressive

Progressive uses Big Data for insurance risk assessment through its Snapshot program, which involves telematics. Here's how it works:

- Progressive collects data on driving behavior, such as speed, braking patterns, and time of day. It tracks drivers' activities through a device plugged into a car.

- This data is analyzed to offer personalized insurance rates based on the individual's driving habits. Safe drivers can receive significant discounts on their premiums. The app also provides driving tips to improve driving habits.

- The data helps Progressive predict the likelihood of future claims and tailor insurance products according to suspected results.

2. John Hancock

John Hancock uses big data analytics for risk and insurance in its Vitality program, which integrates health and wellness data. Since 2018, the company has transitioned towards selling interactive life insurance.

- Policyholders use wearable fitness trackers to monitor their physical activity, diet, and other health metrics.

- Based on the data collected, John Hancock offers dynamic pricing through discounts and rewards for healthy behaviors, such as regular exercise and medical check-ups.

- This approach helps the company better understand the health profiles of its clients for more accurate underwriting and pricing.

3. Allianz

Allianz has implemented big data analytics in risk assessment in the following ways:

- Allianz uses satellite data, weather patterns, and historical event data to model and predict the impact of natural disasters. This helps in underwriting and pricing policies for properties in high-risk areas.

- The company also uses machine learning algorithms to detect fraudulent claims by analyzing patterns and anomalies in the data. This reduces false claims and helps in quicker and more accurate claim settlements.

4. MetLife

MetLife leverages big data for customer insights and operational efficiency:

- The company uses data analytics to segment its customer base more precisely for targeted marketing and personalized product offerings.

- Big data helps MetLife streamline its claims processing by using predictive analytics to assess the validity of claims.

5. AXA

AXA uses big data in several innovative ways:

- AXA incorporates climate data and predictive models for climate risk analysis to assess the impact of climate change on its insurance portfolio, helping to mitigate long-term risks.

- Through its Health Keeper platform, AXA collects and analyzes health data from users, offering personalized health advice and wellness programs, which also feed into their insurance risk assessments. This helps improve personal engagement.

6. Lemonade

Lemonade, a digital insurer, extensively uses big data and AI in customer communications for insurers to:

- Lemonade uses AI bots to collect data from potential customers and instantly underwrite policies based on real-time data analysis.

- Their AI bot, Maya, handles claims processing by analyzing data submitted by customers, detecting fraud, and approving claims in as little as three minutes.

- Lemonade applies principles of behavioral economics to design its user experience.

7. Zurich Insurance

Zurich uses insurance data analytics for risk assessment and management:

- For industrial clients, Zurich uses IoT sensors to collect data on machinery and infrastructure, predicting maintenance needs and preventing breakdowns.

- Zurich analyzes data from wearable devices workers use in high-risk industries to monitor safety practices and reduce workplace accidents.

Challenges for using big data analytics in insurance risk assessment

Big data analytics in insurance risk assessment comes with a myriad of challenges. The key is to be prepared. Here is the list of various challenges to expect:

Data quality and availability

- Data integrity: Ensuring the data collected is accurate, complete, and error-free is crucial. Inconsistent or poor-quality data can lead to incorrect analyses and decisions.

- Data integration: Combining data from multiple sources (e.g., social media, IoT devices, public records) can be complex and time-consuming. Companies need robust systems to integrate and manage disparate data streams effectively.

- Access to relevant data: Some data may be difficult to obtain due to privacy concerns. Companies need to establish agreements and partnerships to access the necessary data.

Data protection and privacy

- Data security: Protecting sensitive customer data from cyber threats is a major concern. Insurance companies must implement strong security measures, such as encryption, secure data storage, and access controls.

- Compliance with regulations: Adhering to data protection laws, such as GDPR in Europe or CCPA in California, is essential. Companies must ensure that their data practices comply with these regulations to avoid legal penalties and maintain customer trust.

- Anonymization and de-identification: When using customer data for analysis, insurers must anonymize or de-identify the data to protect individual privacy while still obtaining valuable insights.

Data analytics and interpretation

- Skilled workforce: There is a high demand for data scientists and analysts with expertise in big data analytics. Insurance companies need to invest in training and hiring skilled professionals to interpret complex data sets accurately. Companies often face a lack of data scientists who have a full understanding of data-centric methodologies.

- Advanced tools and technologies: Developing and maintaining advanced analytics tools requires significant investment. Companies must choose the right technologies and ensure they are scalable and adaptable to evolving needs.

Technological infrastructure

- Scalability: Big data analytics requires substantial computational power and storage capacity. Insurance companies need scalable infrastructure to handle large volumes of data efficiently.

- Integration with legacy systems: Many insurance companies still rely on legacy IT systems. Integrating big data analytics with these systems can be challenging and may require significant upgrades or overhauls.

- Real-time processing: For dynamic pricing and real-time risk assessment, insurers need systems capable of processing data in real-time. This requires advanced data processing capabilities and low-latency networks.

Ethical and legal considerations

- Transparency: Insurers must be transparent about how they use customer data. Clear communication about data collection and usage practices helps build trust and ensures compliance with ethical standards.

- Consent: Obtaining explicit consent from customers before collecting and using their data is essential. Companies must ensure that consent processes are straightforward and communicated.

- Impact on customers: Insurers need to consider the potential implications of big data analytics on customers, such as increased premiums for high-risk individuals. Balancing profitability with fairness and customer satisfaction is crucial.

Organizational challenges

- Change management: Implementing big data analytics often requires significant changes in business processes and culture. Companies must manage these changes effectively to ensure smooth adoption and integration.

- Interdepartmental collaboration: Effective use of big data often requires collaboration across different departments (e.g., IT, actuarial, marketing). Companies need to foster a culture of collaboration and data sharing.

Cost considerations

- Initial investment: The upfront cost of developing big data capabilities can be high, including expenses for technology, infrastructure, and talent acquisition.

- Ongoing maintenance: Maintaining and updating big data systems requires continuous investment in technology and personnel.

Enhancing predictive modeling with big data analytics

Predictive modeling uses wealth of data (both current and historical) to estimate the likelihood of claim approvals and settlement amounts, leading to faster decision-making and more efficient resource allocation. Moreover, predictive modeling for risk assessment leverages big data to enhance accuracy and effectiveness.

Diverse data types such as behavioral, weather, telematics, and IoT data are used to build more comprehensive predictive models. For instance, health insurance companies might use big data analytics to predict chronic diseases like diabetes by analyzing data from electronic health records, genetic information, behavioral data, and wearables.

This integrated approach allows for more accurate assessments and tailored insurance solutions, demonstrating the critical role of data modeling in transforming insurance operations.

Best practices for implementing big data analytics

Are you an insurance business looking to integrate big data into risk analytics and unsure what to start with? Here are the simple best practices to begin your insurance app development .

1. Develop a big data strategy

- Clearly outline the goals and objectives of using big data analytics.

- Create a detailed implementation roadmap that includes short-term and long-term milestones with specific timelines and deliverables.

- Engage key stakeholders to ensure alignment and support for the big data initiatives.

- Put a data integration strategy in place.

2. Invest in infrastructure

- To handle large volumes of data, use cloud-based storage solutions. AWS, Google Cloud, and Azure offer scalable and cost-effective storage options.

- Implement big data technologies like Hadoop, Apache Spark, and NoSQL databases to process and analyze large datasets.

- Invest in high-performance computing resources to support complex data analytics and real-time processing needs.

3. Ensure data quality and management

- Establish a robust data governance framework that defines data standards and procedures for data management.

- Implement data integration tools to combine data from various sources.

- Regularly clean and preprocess data to eliminate inconsistencies.

4. Focus on data security and privacy

- Use robust encryption methods to protect data.

- Implement strict access controls and authentication mechanisms to ensure that only authorized personnel can access sensitive data.

- Ensure compliance with data protection regulations like GDPR, CCPA, and HIPAA.

5. Build a skilled team

- Recruit data scientists, analysts, and engineers with expertise in big data analytics.

- Provide ongoing training and development opportunities to update the team with the latest tools and best practices.

- Help existing underwriters develop technical and analytical skills for handling big data.

- Foster collaboration between data experts and business units to ensure that analytics initiatives are aligned with business needs.

6. Utilize advanced analytics tools

- Invest in machine learning platforms and tools such as TensorFlow, PyTorch, and SAS for predictive modeling and advanced analytics.

- Use data visualization tools like Tableau, Power BI, and Qlik to create intuitive and interactive dashboards for data insights.

- Implement automated analytics tools to streamline data processing and analysis to reduce manual effort and improve efficiency.

- Ensure the data is preserved in the proper format for data analysts and underwriters.

7. Emphasize data-driven decision-making

- Promote a culture of data-driven decision-making across the organization. Encourage employees to rely on data insights for strategic and operational decisions even if they do not directly work with managing big data.

- Define and track key performance indicators (KPIs) to measure the success and impact of big data strategies.

- Establish a feedback loop to continuously improve models and analytics based on real-world outcomes and user feedback.

8. Start with pilot projects

- Begin with pilot projects to demonstrate the value of big data analytics. Choose specific areas with clear, measurable outcomes. This will allow you to test big data analytics in insurance risk assessment without investing significant resources.

- Use an iterative approach to gradually scale successful pilot projects across the organization.

- Identify potential risks and challenges early in the pilot phase and develop mitigation strategies.

9. Maintain transparency and ethics

- Ensure transparency in data collection, usage, and analysis processes. Communicate these practices to customers and stakeholders.

- Obtain explicit consent from customers before collecting and using their data for analytics.

10. Measure and optimize

- Evaluate the performance and outcomes of big data initiatives regularly. Use metrics and analytics to identify areas for improvement.

- Optimize models and processes based on new data insights.

- Plan for scalability to accommodate growing data volumes and evolving business needs.

Final thoughts

Big data significantly enhances risk assessment in the insurance industry through various approaches. Benefits include better risk segmentation, more precise underwriting, more effective fraud detection and claims management, and improved customer service. Famous companies across the industry successfully leverage risk assessment with big data.

However, the integration of risk assessment with big data comes with a set of challenges from maintaining data quality and employing skilled professionals to more general organizational challenges. Fortunately, Binariks experts are dedicated to addressing these challenges, providing reassurance about the support available in this complex process.

Companies like Binariks can assist in big data development services and personalized analytics for insurance companies with the following:

- Consulting

- Data infrastructure and data engineering

- Real-time data analytics

- Predictive analytics

- Data visualization

- Analytics integration

Author

Share